SEBI/IMD/DOF-1/OW/19288/2015 July 9, 2015

Subject: Request for a No Action letter under the SEBI (Informal Guidance) Scheme 2003.

(1) This has reference to your letter dated April 07, 2015 wherein you have sought a “no action letter” from SEBI under paragraph 5(i) of the SEBI (Informal Guidance) Scheme, 2003.

Your submissions

In your letter under reference with regard to the proposal of the entity, you have inter-alia represented the following:

(2) The entity is registered with SEBI as a Portfolio Manager and is also registered with the Association of Mutual Funds of India (AMFI) as a distributor of mutual funds.

(3) The business model proposes to counter-balance or set off the client fee with the distribution fee by reimbursing the client an amount equivalent to the distribution fee. The proposal envisages capping the retention of the distribution fee attributable to the investment by a client by an amount equivalent to the client fee accruing from the client. Thus, the entity would charge the client a fixed percentage of advisory fees based on the total assets under management of each client under the head of client fee. As a distributor of financial instruments, the entity would receive commission from the issuer of the financial product as distribution fee

(4) Where the distribution fee earned would be equal to the client fee accruing from the client, the entity would set off the same from the client fee. In case, the distribution fee earned would be higher than client fee accrued, then the entity would retain only such amount of distribution fee that is equivalent to the client fee accruing. Likewise when the distributor fee earned would be lesser than the client fee accrued, the entity would charge the client the difference between the client fee accrued and the distribution fee earned

Clarifications sought by you

(5) In light of these submissions, you have requested SEBI to issue a ‘No-action letter’ under paragraph 5 of the Informal Guidance Scheme stating that proposed business model will not be construed as a violation of regulation 15 (2) of the SEBI’s Investment Advisers Regulations and of SEBI’s circular no. SEBI/IMD/Cir. No. 8/174648/2009 dated August 27, 2009

Our comments

The submissions made in your letter have been considered and without necessarily agreeing with your an lysis, our views on the issues are as under:

(6) SEBI Circular no. SEBI / IMD / Cir. No. 8 / 174648 / 2009 dated August 27, 2009, which applies to mutual fund distributors and specifies the code of conduct to be followed by the intermediaries of mutual funds wherein, Clauses 13 and 14 of such code of conduct, may be referred to which, read as follows:-

“13. When marketing various schemes, remember that a client’s interest and suitability to their financial needs is paramount and that extra commission or incentive earned should never form the basis for recommending a scheme to the client.

“14. Intermediaries will not rebate commission back to investors and avoid attracting clients through temptation of rebate / gifts etc.’

(7) The business model proposed by you, indirectly provides for rebating commission back to investors, which is not in the interest of market for investors. The same may also encourage mis-selling of products and also result in anti-competitive practices thereby harming the growth of small distributors. Furthermore, the proposal is inconsistent with the code of conduct specified for intermediaries of mutual funds, as stated above

(8) As regards the guidance sought on the applicability of the SEBI (Investment Advisers) Regulations, 2013 (IA Regulations) our comments are as below:

A Portiolio Manager registered under the SEBI (Portfolio Managers) Regulations, 1993, which provides any investment advice to its clients incidental to their primary activity, is entitled to exemption from obtaining registration as an “investment adviser” under Regulation 4 (g) of the SEBI IA Regulations provided that such an intermediary complies with the general obligation(s) and responsibilities as specified in Chapter III of the IA Regulations titled “General Responsibility.”

(9) The relevant provisions of the A Regulations titled “General Responsibility” under Regulation 15 provide as follows

(a) 15 (2)An investment adviser shall not receive any consideration by way of remuneration or compensation or in any other form from any person other than the client being advised, in respect of the underlying products or securities for which advice is provided;

(b) 15 (3) An investment adviser shall maintain an arms-length relationship between its activities as an investment adviser and other activities;

(c) 15 (4) An investment adviser which is also engaged in activities other than investment advisory services shall ensure that its investment advisory services are clearly segregated from all its other activities.

(10) It may Iso be noted that in terms of Regulation 22 of the IA Regulations titled “Segregation of execution services”, those investment advisers which are banks, NBFCs and body corporate, providing distribution or execution services to their clients are required to keep their investment advisory services segregated from such activities. This is subject, inter alia to the proviso that all fees and charges paid to distribution or execution service providers by the client are paid directly to the service providers and not through the investment adviser

(11) In view of the aforesaid provisions, your proposed business model, where the advisory fees and the distribution fees are being sought to be counter balanced or set off, would run contrary to the provisions set out in Regulation 15 read with Regulation 22 of the IA Regulations. Further as statutorily required, both the advisory and distribution and execution activities are required to be clearly segregated from each other. However, the instant proposal would lead to merging of the activities and possible conflict of interest.

(12) This position is based on the representation made to the Division in your letter under reference. Different facts or conditions might require a different result. This letter does not express any decision of the Board on the questions referred.

In light of the aforesaid points, your request for a no action letter for the proposed business plan cannot be accessed to.

Barnali Mulherjee

General Manager

Request letter from Avendus

Re: Request for a No Action Letter under the SEBI (Informal Guidance) Scheme, 2003.

Dear Sir/Madam,

Avendus Wealth Management Pvt. Ltd. (AWMPL) is seeking guidance of SEBI by way of No Action Letter under Paragraph 5(i) of SEBI (Informal Guidance) Scheme, 2003.

We hereby state that the request does not fall within the points set out in paragraph 8 of the said scheme.

A. BACKGROUND AND MATERIAL FACTS

- AWMPL is a company incorporated under Companies Act, 1956. AWMPL is engaged in the business of wealth Management.

- AWMPL is registered with SEBI as a Portfolio Manager under the SEBI (Portfolio Manager) Regulations, 1993 (registration No. INP000003625). As a distributor of Mutual Funds, AWMPL is also registered with AMFI.

PROPOSED ACTIVITY

As a Portfolio Manager, AWMPL advises its clients on discretionary, non-discretionary and advisory bases. AWMPL proposes to charge its clients a fixed percentage of advisory fees based on the total assets under management of each client (“Client Fee”).

AWMPL, as a distributor of all types of financial instruments including but not restricted to mutual funds, structured products, alternative investment funds, third party portfolio management schemes, private equity funds, etc. (“Financial Products”), may receive commission from the issuer of such Financial Products ( Distribution Fee”).

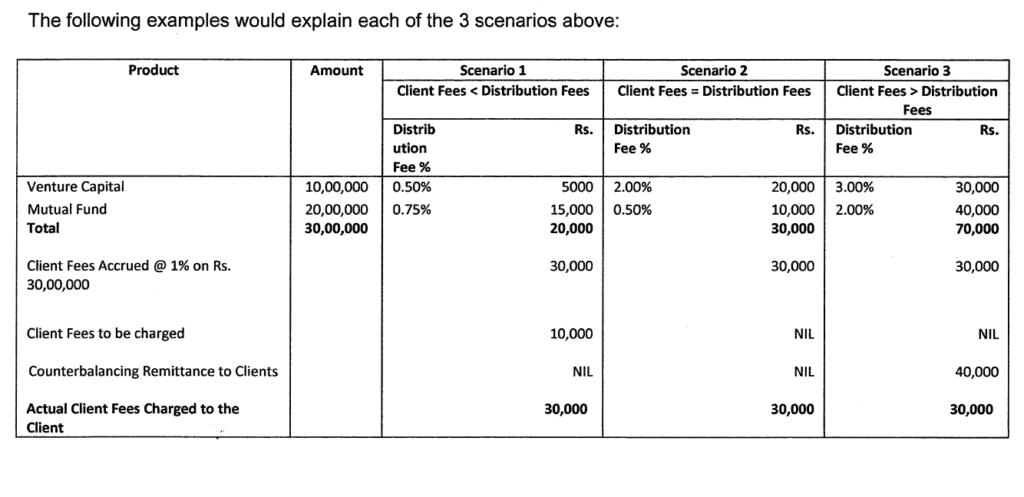

The Distribution Fee would be an income stream that is separate, distinct and in addition to the Client Fee. In furtherance of interests of investors who are clients, AWMPL proposes to counter-balance the Client Fee with the Distribution Fee by reimbursing any amounts equivalent to the Distribution Fee AWMPL proposes to cap the retention of Distribution Fee attributable to the investment by a client by an amount equivalent to the Client Fee accruing from the Client. The same is explained below.

AWMPL would compare the Distribution Fee earned and attributable to the distribution of Financial Products to a client with the Client Fee accruing from the Client. To the extent that the Distribution Fee earned is equal to the Client Fee accruing from that client, AWMPL would set off the same from the Client Fee. Therefore, where the Distribution Fee earned is lesser than the Client Fee accrued, AWMPL would actually charge from the client only the differential between Client Fee Accrued and Distribution Fee earned. Likewise, where the Distribution Fee earned is higher than the Client Fee accrued, AWMPL would retain only such portion of the Distribution Fee that is equivalent to the Client Fee accruing.

The following examples would explain each of the 3 scenarios above:

B. APPLICABLE LEGAL PROVISIONS

Regulation 4(g) of the SEBI (Investment Advisers) Regulations, 2013 (“Investment Adviser Regulation “) exempt SEBI registered Portfolio Managers from registration for their investment advice activity while requiring adherence mutatis mutandis to the Chapter III of the Investment Advisers Regulations.

Regulation 15(2) in Chapter III of the Investment Advisers Regulations states as under:

“An investment adviser shall not receive any consideration by way of remuneration or compensation or in any other form from any person other than the client being advised, in respect of the underlying products or securities for which advice is provided.”

The intention of this provision is to avoid conflict between the interest in servicing the client who is advised, and the interest in distributing Financial Products for the manufacturer of the products.

In case of mutual funds, AWMPL has clients to whom it provides advisory and execution services. These serv es are duly segregated in compliance with SEBI’s requirements in the Investment Advisers Regulations. To be able to effectively advise the clients and track the performance portfolio of its clients (and disseminate to them), the investments are required to be made through the AMFI provided ARN code of AWMPL. The investment made through this code automatically entitles AWMPL to receiving transaction feeds from the Mutual Fund registrars and consequently to commissions from Mutual Funds.

In terms of the structure proposed, it is envisaged by AWMPL that the interests of the Client in terms of the obligation to pay the Client Fee overrides the interests of AWMPL in earning the Distribution Fee. Meeting, the spirit of Regulation 15 above, conflict of interest would be avoided in all scenarios since the maximum earning by AWMPL would always be the very same, thereby eliminating any incentive for AWMPL to make a client buy Financial Products in order to maximize the Distribution Fee. In the proposed system, AWMPL would not gain anything as the Distribution Fee anything more than what the Client would in any case have to pay as Client Fee for advice rendered.

This proposal would also aid transparency and would serve the clients better since the alternative of clients being asked to invest directly without using AWMPL’s ARN Code would inconvenience the clients ar d also be an impediment to effective performance monitoring by AWMPL.

The intent of AWMPL and the real meeting of SEBI’s regulatory objective is borne out by the contents of ‘SEBI’s Circular no. SEBI / IMD / Cir. No. 8 / 174648 / 2009 dated August 27, 2009, which has laid down the Code of Conduct to be followed by the intermediaries of mutual funds (“Circular”).

The relevant extracts from the Circular are reproduced herein below for your ready reference:

“13. When marketing various schemes, remember that a client’s interest and suitability to their financial needs is paramount and that extra commission or incentive earned should never form the basis for recommending a scheme to the client.

14. Intermediaries will not rebate commission back to investors and avoid attracting clients through temptation of rebate / gifts etc.”

The intent of AWMPL is to recommend mutual funds and other financial products to its clients based on their investment strategies and investment objectives and not with an objective to earn extra commission or incentive. Such intent is demonstrated by taking away the earnings of Distribution Fee to the extent it is in excess of the Client Fee. Therefore, AWMPL would only charge a fixed amount of Client Fee to its clients irrespective of the amount of Distribution Fee it receives for distributing the Financial Products.

AWMPL proposes to cap the retention of Distribution Fee attributable to the investment by a client by an amount equivalent to the Client Fee accruing from the Client.

AWMPL is aware of the market practices and the concerns of SEBI while releasing the Circular with the intention that the Portfolio Managers should only promote and distribute genuine Financial Products and not Financial Products simply offering huge amounts of commissions.

In the proposed business model proposed by AWMPL in section B above, AWMPL in no event would earn more than what is contractually agreed with the client. Since AWMPL does not propose to retain any extra incentive, AWMPL believes that there cannot be any potential conflict of interest while offering different Financial Products to its clients. Further, according to AWMPL, such a proposal is in the interest of its clients as it is the clients who are expected to eventually benefit from such a proposal.

C. REQUEST

(1) Given the proposed business model and in light of the applicable legal provisions, AWMPL hereby seeks SEBI’s confirmation regarding the proposed business model whereby AWMPL retains distribution fee only to the extent of the client fee from its PMS clients, remits excess over client fee (if any) to the clients and recovers shortfall in client fee (if any) from the clients. The confirmation is sought in the form of a No Action Letter under paragraph 5 of the Scheme stating that the proposed business model will not be construed as a violation of Regulation 15(2) of SEBI’s Investment Advisers Regulations and of SEBI’s Circular no. SEBI / IMD / Cir. No. 8 / 174648 / 2009 dated August 27, 2009

(2) As this is a proprietary business model and would be easy to copy if made public, AWMPL requests SEBI to keep the same as strictly confidential.

(3) A copy of the Circular is annexed hereto for your ready reference.

(4) We sincerely trust that the above information meets your application requirements and look forward to receiving your reply to the above at the earliest, which shall be critical for our business plan.

Enclosed herewith is the demand draft for a sum of Rs. 25,000/- dated April 8, 2015 drawn on Citibank payable to SEBI, Mumbai.

Should you need any further information, please feel free to contact the undersigned on [+919004669630] or [email protected] at AWMPL.

Thank you for your consideration

Kartik Kini

Chief Administrative Officer

{kind=link}

{kind=link}