WTM/AN/IVD/ID8/29988/2023-24

SECURITIES AND EXCHANGE BOARD OF INDIA FINAL ORDER

UNDER SECTIONS 11(1), 11(4), 11(4A), 11B(1) AND 11B(2) OF THE SECURITIES AND EXCHANGE BOARD OF INDIA ACT, 1992

In respect of:

Noticee No. | Noticee name | PAN |

1. | R. Senthil Kumar | BHDPS1290M |

2. | Geetha N. | BSYPG8237Q |

3. | Prakash V. | AOZPP6915J |

4. | Geetha V. | CGDPG9601A |

(The aforesaid entities are hereinafter individually referred to by their respective names/ Noticee nos. and collectively as “Noticees”)

In the matter of front running activities by certain entities connected with Trustline Holdings Pvt. Ltd. – PMS and Trustline Deep Alpha – AIF

A. BACKGROUND

1. Alert system of Securities and Exchange Board of India (“SEBI”) generated front running alerts with respect to certain entities suspected to be front running the trades of Trustline Holdings Pvt. Ltd. – Portfolio Management Service (“Trustline PMS”) and Trustline Deep Alpha – Alternative Investment Fund (“Trustline AIF”) (collectively referred to as “Big Client” / “Trustline”).

2. SEBI conducted an investigation for the period from May 01, 2017 to June 30, 2022 (“Investigation Period” / “IP”), to ascertain whether certain entities have front run the trades of Big Client and have violated the provisions of the Securities and Exchange Board of India Act, 1992 (“SEBI Act”) and regulations framed thereunder including SEBI (Prohibition of Fraudulent and Unfair Trade Practices Relating to Securities Market) Regulations, 2003 (“PFUTP Regulations”).

3. During the investigation, it was found that Noticees 1 and 3 were employed with Trustline. Noticee 1 was trading in his spouse’s trading account (Noticee 2) using non-public trading information of Trustline, and further, he would communicate such information to Noticee 3, who basis such information was trading in his account and his mother’s trading account (Noticee 4). Therefore, it was found that the Noticees were front running the trades of Trustline. Based on the investigation, SEBI passed an impounding order cum show cause notice dated December 19, 2022 (“Interim Order cum SCN”) with respect to the Noticees inter alia restraining them from buying, selling or dealing in the securities market or associating themselves with securities market, either directly or indirectly, in any manner whatsoever till further directions. Further, the Noticees were made liable to deposit an amount of Rs. 57,66,221 in an escrow account being the alleged unlawful gains.

B. INTERIM ORDER CUM SCN, REPLY, HEARING AND CROSS-EXAMINATION

4. INTERIM ORDER CUM SCN

The prima facie conclusion arrived at in the Interim Order cum SCN is as follows:

4.1 Noticees 1 and 3 were employed at Trustline during the IP and used to operate from the same office premises of Trustline. Noticee 2 is the wife of the Noticee 1. Noticee 4 is the mother of the Noticee 3. Trustline vide email dated May 26, 2022 has submitted that amongst others, Noticee 1 in his role of operations and dealing was involved in the flow of information from decision-making to placing orders till execution of the trades.

4.2 Trustline AIF placed its trades through the trading member, Integrated Enterprises (India) Private Limited (“IEIPL”), and Trustline PMS used to place its trades through IEIPL as well as through Kotak Securities Limited (“Kotak”). ODIN server reports (trade file) submitted by Trustline for the period from March 30, 2017 to October 14, 2022 provides that during the Investigation Period, amongst others, the orders for Trustline were punched from ODIN user ID 29502 (ODIN is a software provided by the brokers for placing orders). Vide email dated October 18, 2022, Trustline has further submitted that Noticee 1 was placing orders for Trustline from the ODIN software through the above noted user ID 29502 during the period from July 28, 2017 to September 23, 2022. Kotak vide emails dated September 14 and 21, 2022 has confirmed that amongst others, Mr. R Senthil Kumar (Noticee 1) and Mr. Prakash V (Noticee 3) were placing orders for Trustline during the period from May 01, 2017 to June 30, 2022.

4.3 During the investigation, summons was issued to the Noticees. Noticees 1 and 3 appeared before the investigation officer and their statements were recorded on oath. In his deposition on August 25, 2022, Noticee 1 has inter alia submitted that:

(i) Noticee 1 being the operations manager cum dealer would supervise the trading activities of Trustline and he would get information of impending orders to be placed on behalf of Trustline.

(ii) Noticee 1 was trading in his spouse’s account (Noticee 2).

(iii) On the basis of such information, he was giving tips to Noticee 3 who was working as an office assistant in Trustline.

(iv) Based on the said tips, Noticee 3 would trade from his account and his mother’s account (Noticee 4).

(v) Profits earned by Noticee 3 by trading through his and Noticee 4’s account were shared equally between Noticees 1 and 3. Noticee 3 would transfer Noticee 1’s share of profit either to his account or account of a third person (Mr. Ranjith / Mr. Stalin) or pay in cash.

Further, Noticee 3 has also admitted (iii) to (iv) stated above in his statement recorded on oath before the Investigating Authority on August 01, 2022. During the investigation, it was inter alia observed that cumulatively through various transactions, an aggregate amount of Rs 10,89,909 was transferred from bank account of Noticee 3 to bank accounts of Noticee 1.

4.4 Thus, Noticee 1 was found to be in possession of non-public sensitive information about the impending trade orders of Trustline, which he obtained by virtue of his employment with Trustline as the operation manager cum Noticee 3 receiving tips of impending orders of Trustline from Noticee 1, trades executed basis such tips and sharing profits out of trades so executed in the trading account of Noticees 3 and 4 are evident from WhatsApp chats exchanged between the Noticees 1 and 3 and the order logs obtained during the investigation.

4.5 From the KYC details of the trading account of Noticee 2 which mentions email ID of Noticee 1, statement given by Noticee 1 on oath to SEBI on August 25, 2022 and affidavit dated September 13, 2022 given by Noticee 2, it was observed that Noticee 1 was placing orders and executing trades in account of Noticee 2. Similarly, from KYC details of the trading account and bank account of Noticee 4 which provides email for correspondence and mobile no. of Noticee 3, statement given by Noticee 3 on oath to SEBI on August 01, 2022, email of trading member of Noticee 4 on September 07, 2022 stating that Noticee 4 has authorized Noticee 3 to place orders from her account and affidavit dated September 06, 2022 submitted by Noticee 4, it was observed that Noticee 3 was placing orders and executing trades in his account and account of Noticee 4.

4.6 An analysis of the orders executed from the accounts of Noticees 2 to 4 revealed that the order for the first leg of the intra-day trade (the front running leg) was placed from these trading accounts just prior to the impending orders of the Big Client and the second leg of the intra-day trade (squaring off trade) was set in motion by the front runners by placing the orders before the last tranche of the impending orders by the Big Client, in order to square off the position to earn profits. The said trades have followed either a Buy-BuySell (BBS) pattern or a Sell-Sell-Buy (SSB) pattern.

4.7 An analysis of common scrip days of front runners with the Big Client was carried out during the Investigation Period. The following is a summary of the trading profiles of the front runners e., Noticees no. 2 to 4 and the common scrip days they shared with the Big Client, i.e., Trustline:

Table 1

Front runners | Number of instances of trades executed during the Investigation Period | Common scrip days with Trustline | % |

Noticee 2 | 1,317 | 356 | 27.03 |

Noticee 3 | 329 | 174 | 52.89 |

Noticee 4 | 1,335 | 760 | 56.93 |

4.8 For calculation of unlawful proceeds, number of scrip days where the Noticees have day traded and commonly traded with the Big Client and have earned a positive square off earning of Rs. 1 or more, have been taken into consideration and the profit so earned in the account of respective Noticees have been ascertained as below:

Table 2

Name of the front runner | Total unlawful gains (Rs) |

Ms. Geetha N. (Noticee 2) | 12,10,234 |

Mr. Prakash V. (Noticee 3) | 5,40,196 |

Ms. Geetha V. (Noticee 4) | 40,15,791 |

Total | 57,66,221 |

5. REPLIES

5.1 Replies of Noticee 1 submitted vide email dated April 06, 2023 and July 6, 2023 are summarized below:

5.1.1 Regarding email submitted by Trustline dated May 26, 2022 wherein it submitted list of 5 persons who were involved in flow of information from decision making to placing orders till execution of trades, Trustline has withheld vital information. The table only pertains to the year 2022, while it does not disclose about the existence of one Mr. Sathishkumar, (Dealer). While the ODIN dealer terminal login accounts were held in two different names, the orders were placed by Mr. Vijaykumar, Mr. Sathish Kumar, Mr Ramesh Kumar and some other senior officials of Trustline. Mr. Sathish and Mr. Vijayakumar (Dealer & Coordinator) used his terminal to place the orders and had information about the impending orders to be placed till 2019. Only after the demise of Mr. Sathish in 2019, Noticee 1 was elevated to the position of operations manager. The ODIN dealer terminal was opened in his name only in July, 2021. However, his job description was to manage and oversee the entire operation. The office setup is small and open which virtually enables every individual to be aware of the information relating to impending shares. The Trustline management has concealed the said facts in order to escape the liabilities arising out of the violations therein. In quasi-judicial proceedings what is to be seen is preponderance of possibility and the facts stated above shows that many others had the confidential information besides the authorized individual and the accounts were held in the name of different dealer. Therefore, the theory in the Interim Order cum SCN that Noticee 1 was the mastermind is untenable because Noticee 1 was not the only custodian of the confidential information.

5.1.2 Noticee 3 in his cross examination has admitted the following:

“Q7. I put it to you, that the Trustline office is a small office.

Ans. Yes, its a small office in a big building on the 3rd floor.

Q8. Are the chambers close to each other? Are they open?

Ans. Yes, they are open.

Q10. Can one view the contents of the Computer?

Ans. While one is walking around, one can view the contents of the computer”

The above admission of Noticee 3 in his cross examination would show that there was no separate dealer room and the computers containing confidential information were kept open in a small office and the access to such confidential information were in the hands of many. Noticee 3 has been acting in concert with the management of Trustline and in bailing them out for violation of SEBI Regulations, he has imputed Noticee 1. This is clear from the fact that Noticee 3 during his online cross examination went intermittently missing and when asked about it, he admitted to have been in phone calls during cross examination, thereby establishing the concerted activities.

5.1.3 Noticee 3 was not able to identify the WhatsApp Chats produced during the cross examination proceeding. The Hon’ble Supreme Court in Roop Singh Negi vs. Punjab National Bank reported (2009) 2 SCC 570, held that mere production of document is not enough, but the document produced in the evidence has to be proved by examining witnesses, and on this ground alone the impugned orders need to be set aside. Therefore, the WhatsApp chats cannot be considered as an evidence when Noticee 3 could not speak through the contents of the documents.

5.1.4 As to information given by Trustline (for the period July 28, 2017 to September 23, 2022) and Kotak (for the period May 01, 2017 to June 30, 2022), that trades of Trustline were being punched in from ODIN user ID 29502 by Noticee 1, the said information is false and misleading. The investigation was conducted in a biased manner and in a manner not known to law. Statements of Noticee 3, are misleading and perjurious. When Noticee 1 was investigated, he was enquired in a biased manner and answers were recorded on coercion at the convenience of the Investigation Officer, in such a way as to align statements with that of Noticee 3.

5.1.5 Various statements made by Noticee 3 are contradictory to documentary evidence. For illustration, statement of Noticee 3 made in his examination on oath dated August 01, 2022, in which, in response to question 8, he has stated “I took loan of Rs. 3,00,000/-from axis bank in 2016-17, on the advice of Mr R. Senthil Kumar” and in response to question 11 he has stated that “I opened my account in year 2016-17”. From the above, it is clear that Noticee 3 opened his account in the year 2016-17. However, his response to question 8 is misleading and is made with an attempt to impute Noticee 1 as the abettor. Noticee 1 got acquainted to Noticee 3 only after he joined Trustline in June, 2017. The true copy of the order appointing Noticee 1 in Trustline is annexed as annexure 6 to the reply. The said document expunges the statement of Noticee 3 and the statements of Trustline and Kotak that Noticee 1 has been placing orders since May 2017, which is not possible in view of the fact that he joined Trustline only after June 2017. Noticee 3 has been working in Trustline since 2013 and he has knowledge of impending big orders through Mr. Sathish Kumar.

5.1.6 The bank transactions between Mr. Prakash (Noticee 3) and Late Mr. Sathish would establish their connections in front running till 2019. The said bank statement is annexed as annexure 7 to the reply. This clearly shows that the imputation of Noticee 1 being the mastermind as per the Interim Order cum SCN is baseless and the conclusions are drawn on surmises and false imputations made by Noticee 3.

5.1.7 Noticee 1’s statement recorded on oath dated August 25, 2022, stating the following were obtained in coercion in order to corroborate the statements in line with that of Noticee 3 and falsely impute him.

(i) Noticee 1 was supervising the trading activities of Trustline;

(ii) He had credentials of “Miles System” of Trustline;

(iii) Being the operations manager cum dealer, he was supervising the trading operations and he used to get information of impending orders to be placed on behalf of Trustline;

(iv) On the basis of information about the impending orders of Trustline he used to give tips to Noticee 3;

(v) Based on his tips, Noticee 3 used to trade in scrips from his own trading account as well as from the trading account of Noticee 4;

(vi) Profits earned from such trades executed through the trading accounts of Noticees 3 and 4, were shared in the ratio of 50:50 between him (Noticee 1) and Noticee 3.

5.1.8 On some occasions, Noticee 3 paid Noticee 1 for guidance provided by him in the purchase of shares. The same can only be attributed to his 15 years of experience and knowledge and not to his knowledge of impending orders of Trustline. Noticee 3 was aware of all the impending orders just as Noticee 1 or even before him which is apparent from the WhatsApp conversation between them which was placed before SEBI by Noticee 3. An illustrative explanation of WhatsApp conversations is annexed as Annexure 8 to the reply. The modus operandi of Noticee 3 is that he has prior information due to the small and open office set-up and he either gets the information confirmed through Noticee 1 or someone else in person or through WhatsApp. The highlighted messages would show that Noticee 3 was aware of the impending orders and he was confirming it with Noticee 1 which makes it clear that Noticee 3 had prior information from some other source.

5.1.9 Regarding the finding in Interim Order cum SCN that during the Investigation Period, cumulatively a total amount of Rs 13.67 lakhs was withdrawn from the bank account of Noticee 2 maintained with State Bank of India through ATM withdrawal and Rs. 3.3 lakhs were transferred to the accounts of Noticee 1, it may be noted that apart from trading, both Noticees 1 and 2 were earning in their respective jobs. Therefore, the salary was also credited to their account. Besides, both Noticees 1 and 2 have maintained proper accounts and have been filing income tax returns every year attached as annexure 9 and 10 to the reply. The transfer of Rs. 3.3 lakhs was made for the purposes of EMI for pending loans and charges. If Noticee 1 had any intention to have unlawful gains, he would not have disclosed the income and filed the returns.

5.1.10 The imputation that Noticee 2’s account, maintained by Noticee 1 had a huge profit to the tune of Rs. 12,10,234 is incorrect. The table below will demonstrate the actual profits and loss situation:

Table 3

FY | Gain | Loss | Net Gain |

2017-18 | 24110.73 | 3390.54 | 20720.19 |

2018-19 | 16782.13 | 45333.11 | -28551 |

2019-20 | 404910.8 | 61686.31 | 343224.5 |

2020-21 | 331142.4 | 44028.95 | 287113.4 |

2021-22 | 406473.7 | 206734.9 | 199738.8 |

Total | 1183420 | 361173.8 | 822245.9 |

It is a settled principle that any error in computation/ discrepancy shall be decided in favor of the noticee.

Table 4: Angel pay-in and pay out details

Period | Pay-in | Payout |

01.01.2017 to 31.03.2019 | 274000 | 33552.25 |

01.04.2019 to 31.03.2020 | 401500 | 141000 |

01.04.2020 to 31.03.2021 | 240000 | 385579.2 |

01.04.2021 to 31.03.2022 | 1319440 | 1133269 |

01.04.2022 to 30.06.2022 | 262000 | 266841.5 |

Balance payout on 20.08.2022 |

| 26235.05 |

| 2496940 | 1986477 |

Net Loss | 510462.8 |

|

5.1.11 The above table would show that overall trades have resulted only in loss and virtually had no profits after taking into account all the trades executed in the demat account of Noticee 2 handled by Noticee 1. It further goes on to show that the net result is a loss of Rs. 5,10,462.8.

5.1.12 The usage of definite conclusions in the Interim Order cum SCN that Noticee 1 was in possession of the information of the impending trades of Trustline which was not available in the public domain shows that the authority is prejudiced. A show cause notice cannot contain definite conclusions and should merely intimate the noticee about the charges/ imputations. This position has been settled by the Hon’ble Supreme Court in more than one case including in Oryx Fisheries India Pvt. Ltd. vs. Union of India reported in (2010) 13 SCC 427. The connections alleged in the Interim Order cum SCN between the Noticees, placing of orders by Noticee 3 (in his account as well as of Noticee 4) basis information received from Noticee 1 of impending orders to be placed by Trustline, sharing of profits between Noticees 1 and 3 in 50:50 ratio, is framed based on false statement given by Noticee 3 and statement coercively obtained from Noticee 1.

5.1.13 With respect to WhatsApp chats and trades explained in paragraphs 19, 20 and 21 of the Interim Order cum SCN, the authority has relied on selective WhatsApp conversations provided by Noticee 3 which shows bias. Further, the table in paragraph 20 does not show front running. It is a settled proposition that for an order to constitute front running, the front runner’s order should be placed before the big client’s order. In the instant case, the order has been placed after the order of big client, at which time information is no longer confidential information and is open to the public. With respect to trades executed on August 03, 2021 detailed in paragraph 21 of the Interim Order cum SCN, the order of the alleged front runner was placed at 11:22:20 while the order of big client on the same day was placed at 11:06:47. Therefore, such an order cannot be construed as front running or as any other unfair trade practice.

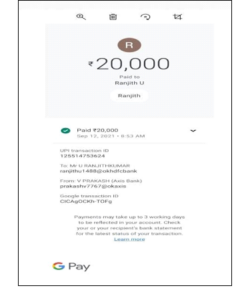

5.1.14 Regarding WhatsApp chats between Noticees 1 and 3 on September 12, 2021 and April 10, 2022 and subsequent payments from Noticee 3 to Mr. Ranjit U, it is true that there were transactions between Noticees 1 and 3, it is denied that the said transactions were for the information about impending orders of Trustline. Mere presence of transactions does not establish the intention or the commission of the act. The transactions were as agreed between Noticees 1 and 3 for helping Noticee 3 with the securities market with the knowledge possessed by Noticee 1. The total transaction between Noticees 1 and 3, both in cash and through bank transactions, is Rs 12,50,000.

5.1.15 Annexure 8 to the reply, WhatsApp conversations, more particularly “Singapore nifty 300 points down by 2 percent… US markets down by 3 to 4 percent and nasdaq down by nealry 5 percent… Tighten your seat belts and get ready for today high volatile expiry trades.” Shows that the messages were a general caution given by Noticee 1 to Noticee 3. The selective submission of WhatsApp conversation has created an image of Noticee 1 being a perpetrator. Therefore, it is baseless to state that he has capitalised the information possessed by him in his official capacity.

5.1.16 It is true that Noticee 1 was operating the account of Noticee 2 by a power of attorney dated July 24, 2017 authorising him to handle the trading account owing to his years of experience and knowledge in securities market and not solely basis his knowledge of impending orders of Trustline. In absence of any knowledge or intent, it cannot be said that Noticee 2 has facilitated the alleged front running.

5.1.17 Regarding the trades executed from account of Noticee 2 by Noticee 1 following a BBS and/or SSB pattern around the timing of placement of orders of the Big Client as detailed in paragraphs 43 to 48 of the Interim Order cum SCN, the entire allegation of front running is merely on the basis of surmises and false statement of Noticee 3. Further, there is a serious computation error in the shares that are alleged to be front run. At any point in time, any shares placed after the purchase of big client’s order, can never be termed as front running. The office set-up being small and open, virtually every individual had access to the confidential information of Trustline including Noticee 3, therefore, the allegation of Noticee 1 being the mastermind and tipping noticee is baseless. The table below explains the error of SEBI in computing the alleged front running:

Table 5

S. No. | Description | Amount (Rs.) |

1 | Alleged profit by front running as per the showcause notice | 12,10,234 |

2 | Error in computation as per Annexure 11 | 3,87,988 |

3 | Net loss suffered in overall trading for the FY 2017 to 2022 | (5,10,462) |

4 | Total gain | 8,22,246 |

5.1.18 The profits should be calculated taking into the account the losses suffered failing which the profits so arrived is not actual profits but only illusionary ones. Hon’ble Supreme Court in SEBI vs. Shri Kanaiyalal Baldevbhai Patel and Ors., reported in (2017)15 SCC 1 has observed as follows: “As per the Major Law Lexicon by P Ramanatha Aiyar (4th Edition 2010), ‘front running’ is defined as under: Front running – Buying or selling securities ahead of a large order so as to benefit from the subsequent price move”. The above ruling is squarely applicable to the present case and the working showing the error in computation is annexed as annexure 12 to the reply.

5.1.19 Regarding percentage of common scrip days of alleged front runners with Trustline, 27% of total order match by Noticee 2 is purely coincidental while orders of Noticees 3 and 4 matched to an extent of 52% to 57%. Further, while trading from account of Noticee 2, no confidential information which was entrusted to Noticee 1 in professional capacity was used.

5.1.20 No other disciplinary actions are pending before SEBI or before any other regulatory body. In compliance of the Interim Order cum SCN, Noticee 1 has deposited Rs. 10,49,969 into the escrow account including the amount secured by selling the movable asset, namely the car mentioned in the affidavit declaring the assets of Noticees 1 and 2.

5.2 Reply of Noticee 2 submitted vide letter dated January 24, 2023/email dated January 27, 2023 is summarized below:

5.2.1 On July 24, 2017, Noticee 2 had issued a letter to her sub-broker (Angel Brokering Co.) authorizing her husband to deal with her trading account. All trades were executed by Noticee 1 via mobile application of Noticee 1. Relevant trade logs with IP address of mobile phone is enclosed.

5.2.2 She has no knowledge about trading and did not have an intention to front run. No mens rea can be attributed to Noticee 2 and charges against her should be dropped.

5.3 Reply of Noticee 3 submitted vide email dated February 01, 2023 and July 10, 2023 is summarized below:

5.3.1 Noticee 3 was working as an office assistant under Noticee 1, where Noticee 1 was his immediate superior, and he had to act only as per his instructions. It is admitted by Noticee 1 in his deposition, that he alone had login ID and password of Noticee 3’s trading account. Noticee 1 used to get all information. As an obedient subordinate, Noticee 3 had to carry out his instructions as otherwise it would have cost him his job. Trading operations were supervised only by Noticee 1 and Noticee 3 acted as per his instructions. Amounts were transferred only to the account of Noticee 1 and his men.

5.3.2 Noticee 3 admits that he received money in his and his mother’s account (Noticee 4), however, it was for carrying out Noticee 1’s instructions. Noticee 3 did not have any intention to cheat any person.

5.3.3 Noticee 3 joined Trustline in Chennai on August 07, 2013, as an office boy. He was given basic administrative duties, which mainly included serving beverages to guests or staff, collecting and distributing couriers or packages among workers, and any other duties directly assigned by Mr. Arunagiri, the Chief Executive Officer (CEO) of the company. On July 30, 2022, he resigned from his job as office boy upon the CEO’s approval due to personal problems. Throughout his work tenure at Trustline, he only performed the aforementioned duties as an office boy.

5.3.4 In 2014, Noticee 3 was co-working with Noticee 1 who was working as an assistant manager (operations) in Trustline. In 2015, Noticee 1 started his own sub-brokerage firm registered with Angel Broking Ltd. (now Angel One). In 2016, he collected Rs. 1,40,000 from Noticee 3, promising to generate good returns. After few months, Noticee 1 declared that the money Noticee 3 had given to him was lost.

5.3.5 After rejoining Trustline in 2016-2017, Noticee 1 gave a guarantee to recover the loss incurred with Noticee 3’s money by providing him with research tips (stock buy and sell recommendations). Noticee 1 said that he would be charging commission for the stock tips he was providing Noticee 3, since the recommendations were based on his own research, and he was also charging similar fees to a few other clients he was handling at the time. However, Noticee 3 was unable to execute the research tips provided by him since he is not capable of trading on his own. Noticee 1 insisted that Noticee 3 should open two demat accounts in Sharekhan, one with his name and another with his mother’s name. Pursuant to his request, Noticee 3 shared the user credentials of the two demat accounts with him. After which, Noticee 1 started executing his own research tips by trading in the said demat accounts, on behalf of Noticee 3 and 4.

5.3.6 With regard to Question No. 2 of the cross-examination proceedings, Noticee 1 has stated that he is unable to recollect if he had opened an Angel Broking demat account with Noticee 3’s name under his sub-broker license. He has also denied that he solely handled the given amount. However, Noticee 3 has already enclosed necessary evidence to SEBI, proving that he had opened a demat account using Noticee 3’s name under his subbrokerage and the amount (Rs. 1,40,000) was transferred to the account of ATOM Stock Brokers, as requested by Noticee 1. Also, for Question 4, Noticee 3 has provided necessary evidence to SEBI, proving that Noticee 1 was carrying out his own research for creating stock tips to Noticee 3.

5.3.7 Since Noticee 3 does not have the capacity to collect and produce evidence to substantiate his stance with regard to Question No. 6 of cross-examination, SEBI is requested to investigate further to find out the number of clients to whom Noticee 1 was providing same research tips at the same time when he was handling Noticee 3 as one of his clients. On considering the depositions of Noticee 1, it can be clearly seen that all the misdeeds have been done by Noticee 1 and Noticee 3 has been falsely implicated.

5.4 Reply of Noticee 4 submitted in Tamil vide email dated February 06, 2023 is translated and summarized below:

5.4.1. Noticee 4 neither knows anything about the stock market nor does she have any connection with it.

5.4.2. Her son (Noticee 3) asked Noticee 4 to sign on few papers based on request of Noticee 1, hence, she signed.

6. HEARING

6.1 Noticees were granted hearing opportunity before the undersigned. Noticee 1 appeared on behalf of Noticees 1 and 2 on April 11, 2023. Noticee 1 reiterated that the details shared by him with Noticee 3 were in the nature of expert advice for which he received Rs. 12.5 lakhs from him. The said details cannot be considered as front running tips. One Mr. Sathish was the key person who used to share tips. In any case, dealers of Trustline and Prakash V. used to sit in a small room, where the confidential information regarding the trades to be placed for Trustline was known to everyone sitting in the said room including Noticee 3. He has further stated that the statement given by him to the Investigating Authority on August 25, 2022 on oath was not given under duress.

6.2 Noticee 3 also appeared before me on April 11, 2023 on behalf of Noticees 3 and 4 as Noticee 4 being 59 years old could not attend due to old-age and physical ailments. During the hearing, Noticee 3 stated that he was given tips regarding impending orders of Trustline by Noticee 1 through physical papers, text messages and WhatsApp messages. Previously, when Noticee 1 was working for another company, Noticee 1 had taken funds from Noticee 3 for trading in securities market, which he lost, when Noticee 1 re-joined Trustline, he offered to recover the funds of Noticee 3 by sharing tips of impending orders of Trustline to Noticee 3. It was agreed between them that the profits made through the said tips would be shared between them equally. The distribution of profits was made basis end of month reconciliation. Noticee 3 further stated that he had opened his trading account and of his mother on basis of advice of Noticee 1. He was not under any pressure from Noticee 1 to execute trades basis tips received of impending orders of Trustline.

7. CROSS EXAMINATION

Noticee 1 had sought cross-examination of Noticee 3 with respect to Noticee 3’s statement before the Investigating Authority, SEBI dated August 01, 2022, which was conducted on May 08, 2023. Further, Noticee 3 had sought cross-examination of Noticee 1 with respect to Noticee 1’s statement dated August 25, 2022, which was conducted on June 26, 2023.

C. CONSIDERATION OF ISSUES AND FINDINGS

I have considered the Interim Order cum SCN, replies of the Noticees, and other material available on record. Accordingly, the following issues emerge for consideration in the present matter:

Issue I: Whether the preliminary contentions of Noticee 1 are tenable?

Issue II: Whether the Noticees have front run the trades of Trustline?

Issue III: If the answer to Issue II is in affirmative, whether the Noticees have violated section 12A (a), (b), and (c) of the SEBI Act and regulations 3(a), 3 (b), 3 (c), 3(d), 4(1) and 4(2)(q) read with regulation 2(1)(c) of PFUTP Regulations?

Issue I: Whether the preliminary contentions of Noticee 1 are tenable?

8. I find it appropriate to begin by dealing with the preliminary contention raised by Noticee 1. Noticee 1 has contended that the usage of definite conclusions in the Interim Order cum SCN that Noticee 1 was in possession of the information of the impending trades of Trustline which was not available in the public domain shows that the authority is prejudiced. A show cause notice cannot contain definite conclusions and it should merely intimate the noticee about the charges/ imputations. Reliance has been placed by Noticee 1 on decision of Hon’ble Supreme Court in Oryx Fisheries India Pvt. Ltd. vs. Union of India reported in (2010) 13 SCC 427. I have perused the decision of Oryx Fisheries India Pvt. Ltd. (supra) relied upon by the Noticee 1. The said decision concerns whether procedure adopted for cancelling registration certificate of a company was fair. I note that before cancelling the said certificate, the show cause notice issued to the said company included words such as “convincingly proved” and “proved beyond doubt”, which gave an indication that the authority therein had already up its mind. Further, the order passed for cancelling the certificate was a non-speaking one as it merely stated that the reply of the company was not satisfactory.

9. Contrary to the above, I find that the Interim Order cum SCN at paragraph 63 clearly states that “The prima facie observations/ findings contained in this Order are made on the basis of the material available on record. In light of the alleged violations of the provisions of the SEBI Act, 1992 and PFUTP Regulations, 2003 by the Noticees, this Order shall be treated as a Notice under Sections 11(1), 11(4), 11(4A), 11B (1), 11B (2) and 11(5) of SEBI Act 1992, read with SEBI (Procedure for Holding Inquiry and Imposing Penalties) Rules, 2005, calling upon them to show cause as to why certain directions shall not be passed against them, as proposed hereunder:…”. From the above, the usage of the words “prima facie” itself shows that the findings recorded are based on first appearance or that the findings, on its face, are subject to further evidence or information. Further, Noticees have been called upon to show cause as to why certain directions should not be passed against them i.e, an opportunity was granted to them to refute the material gathered during investigation and the preliminary findings arrived at. Thus, this contention of Noticee 1 is not tenable in the facts of the case.

Issue II: Whether the Noticees have front run the trades of Trustline?

Issue III: If the answer to Issue II is in affirmative, whether the Noticees have violated section 12A (a), (b), and (c) of the SEBI Act and regulations 3(a), 3 (b), 3 (c), 3(d), 4(1) and 4(2)(q) read with regulation 2(1)(c) of PFUTP Regulations?

10. I find that essentially, the issue that requires to be addressed in the present matter is whether the Noticees have front run the impending orders of Big Client, and consequently, violated provisions of the SEBI Act and PFUTP Regulations. The provisions relevant to the present issue are reproduced below:

10.1 SEBI Act

Prohibition of manipulative and deceptive devices, insider trading and substantial acquisition of securities or control.

12A. No person shall directly or indirectly—

- use or employ, in connection with the issue, purchase or sale of any securities listed or proposed to be listed on a recognized stock exchange, any manipulative or deceptive device or contrivance in contravention of the provisions of this Act or the rules or the regulations made thereunder;

- employ any device, scheme or artifice to defraud in connection with issue or dealing in securities which are listed or proposed to be listed on a recognised stock exchange; (c) engage in any act, practice, course of business which operates or would operate as fraud or deceit upon any person, in connection with the issue, dealing in securities which are listed or proposed to be listed on a recognised stock exchange, in contravention of the provisions of this Act or the rules or the regulations made thereunder;

10.2 PFUTP Regulations

3. Prohibition of certain dealings in securities

No person shall directly or indirectly—

- buy, sell or otherwise deal in securities in a fraudulent manner;

- use or employ, in connection with issue, purchase or sale of any security listed or proposed to be listed in a recognized stock exchange, any manipulative or deceptive device or contrivance in contravention of the provisions of the Act or the rules or the regulations made there under;

- employ any device, scheme or artifice to defraud in connection with dealing in or issue of securities which are listed or proposed to be listed on a recognized stock exchange; (d) engage in any act, practice, course of business which operates or would operate as fraud or deceit upon any person in connection with any dealing in or issue of securities which are listed or proposed to be listed on a recognized stock exchange in contravention of the provisions of the Act or the rules and the regulations made there under.

4. Prohibition of manipulative, fraudulent and unfair trade practices

(1) Without prejudice to the provisions of regulation 3, no person shall indulge in a manipulative, fraudulent or an unfair trade practice in securities markets.

*[Explanation.– For the removal of doubts, it is clarified that any act of diversion, misutilisation or siphoning off of assets or earnings of a company whose securities are listed or any concealment of such act or any device, scheme or artifice to manipulate the books of accounts or financial statement of such a company that would directly or indirectly manipulate the price of securities of that company shall be and shall always be deemed to have been considered as manipulative, fraudulent and an unfair trade practice in the securities market.]

(2) Dealing in securities shall be deemed to be a *[manipulative] fraudulent or an unfair trade practice if it involves any of the following:—

(a)…

(b)… ….

(q) any order in securities placed by a person, while directly or indirectly in possession of information that is not publically available, regarding a substantial impending transaction in that securities, its underlying securities or its derivative;

…

* Inserted vide Securities and Exchange Board of India (Prohibition of Fraudulent and Unfair Trade Practices relating to Securities Market) (Second Amendment) Regulations, 2020 w.e.f. October 19, 2020.

Even though the SEBI Act and the PFUTP Regulations do not mention the term “front running”, regulation 4(2)(q) of PFUTP Regulations specifically covers front running transactions. From the above, regulation 4(2)(q) of PFUTP Regulations requires satisfaction of the following two elements: (i) existence of non-public information regarding the substantial order of big client for dealing in securities; and (ii) orders placed by the alleged front runner (directly or indirectly) in advance of the substantial impending order to be placed by big client, while being in possession of the said non-public information.

11. From the above, it can be stated that to classify a trading activity as front running, the following two important factors need to be determined:

(i) First, there should be an information which is not publicly available regarding substantial impending order of big client in a security; and

(ii) Second, the alleged front runners place orders in security (directly or indirectly) while in possession of the aforesaid non-public information in advance of large order to be placed by the big client.

CONNECTION INTER-SE BETWEEN THE NOTICEES AND ACCESS TO NONPUBLIC INFORMATION

CONNECTION INTER-SE BETWEEN THE NOTICEES

12. I note from the material available on record that the Noticees are connected inter alia through family relationship, financial transactions, professional relation and KYC details. The connection of entities in whose accounts front running of impending orders of Trustline was observed and the mode of placing orders are highlighted as under:

Table 6

Entities front running trades of Trustline | Date of account opening and name of the person who had opened the trading account | Mode of order placement and operation of trading account | Connection of front runners with Trustline – PMS & AIF |

Ms. Geetha N (Noticee 2)

| July 24, 2017

Account opened by Ms. Geetha N. | Trading account maintained with Angel Broking Ltd.

Mode of order placement: Internet based trading facility. | Noticee 2 is wife of Noticee 1. Noticee 1 was dealer of Trustline and had information of the impending trades of Trustline (discussed in detail in subsequent paragraphs). |

Mr. Prakash V (Noticee 3) | April 07, 2014

Account opened by Mr. Prakash V. | Trading account maintained with trading member Sharekhan Ltd.

Mode of order placement: Internet based trading facility, mobile application and phone calls. | Noticee 3 and Noticee 1 were employees of Trustline. Noticee 1 was dealer of Trustline and he had information of the impending trades of Trustline (discussed in detail in subsequent paragraphs). Noticee 3 was back office executive of Trustline. |

Ms. Geetha V (Noticee 4)

| November 27, 2017

Account opened by Ms. Geetha V. | Trading account maintained with trading member Sharekhan Ltd.

Mode of order placement: Internet based trading facility, mobile application and phone calls. | Noticee 4 is mother of Noticee 3 who was employed as back office executive of Trustline. |

13. I note from the affidavit submitted by Noticee 2 dated September 13, 2022 (provided as Annexure 13 to the Noticees), that she has stated that Noticee 1 had opened trading account in her name with Angel Broking Ltd. She has further stated that her husband was trading through her account and she had no knowledge about trading in shares. The same is also corroborated by Noticee 1’s affidavit dated September 13, 2022 (provided as Annexure 17 to the Noticees).

14. Further, I note that Noticee 4 vide affidavit dated September 06, 2022 (provided as Annexure 11 to the Noticees), has submitted that Noticee 3 was carrying out trading through her account along with Noticee 1 from 2017 to 2022. She has also stated that she is uneducated and that she has no knowledge about her demat account. The above is also corroborated by Noticee 3 vide his affidavit dated September 06, 2022 provided as Annexure 8 to the Noticees. Additionally, I note that trading member with which Noticee 4 has trading account, Sharekhan Ltd., vide email dated September 07, 2022 has submitted an authorized representative form which states that for client “Geetha Vijaykumar” bearing client code 2146118, the authorized representative is “Prakash V” bearing client code 1614884 e, Noticee 3. The said email was provided as Annexure 10 to the Noticees.

ACCESS TO NON-PUBLIC INFORMATION

15. I find it appropriate to begin by referring to the judgment of Hon’ble SC in SEBI vs. Kanaiyalal Baldevbhai Patel and Ors., (2017)15SCC1, decision dated September 20, 2017, wherein it inter alia held that “…..Confidential information acquired or compiled by a corporation in the course and conduct of its business is a species of property to which the corporation has the exclusive right and benefit, and which a court of equity will protect through the injunctive process or other appropriate remedy. The information of possible trades that the company is going to undertake is the confidential information of the company concerned, which it has absolute liberty to deal with. Therefore, a person conveying confidential information to another person (tippee) breaches his duty prescribed by law and if the recipient of such information knows of the breach and trades, and there is an inducement to bring about an inequitable result, then the recipient tippee may be said to have committed the fraud.”

From the above, I conclude that the information of possible trades of a company is confidential / non-public information.

16. To ascertain whether Noticees 1 and Noticee 3 had access to confidential / non-public information of orders of Trustline, it becomes imperative to examine the flow of information in Trustline from the time the decisions for trading in scrips are taken to the time orders are placed and executed. In this regard, Trustline vide email dated May 26, 2022 (provided as Annexure 1A to the Noticees) has submitted that the following persons were involved from decision making of trades till execution of the trades during the period May 01, 2017 to June 30, 2021:

Table 7

S. No | Name | Role |

1 | Arunagiri N | Fund Manager |

2 | Deepan Sankara Narayanan | Research |

3 | Ramesh Kumar S | Client servicing and dealing |

4 | Senthil Kumar R | Operations and dealing |

5 | Vijayakumar J | Dealing co-ordination |

17. Further, vide email dated October 17, 2022 (provided as Annexure 1B to the Noticees), it has inter alia submitted the sequence of steps from stock finalization to trade execution. It has stated that once research reports are finalized, decision is taken jointly between Principal Officer cum Fund Manager and VP Research to initiate the stock allocation with a specified target price to buy or sell along-with an appropriate portfolio weightage. On a particular day, based on the price movements in the relevant stocks, decision to buy/sell is taken dynamically during the trading hours (decision is taken anytime between 9.15 am to 3.30 pm with no fixed time). This decision is primarily taken by the fund manager and it is communicated verbally to the dealer/ dealer coordinator of Trustline through a faceto-face discussion or through call. Post this, email for exposure is sent to the risk-team of the broker, once the risk team of the broker clears and sets the exposure limit for the stocks in terminal (ODIN) server, then the dealer or dealer coordinator punches the order and executes the trades in the ODIN terminal (system on which ODIN is loaded). For trade execution and tracking, Trustline uses the ODIN platform provided by its broker e., IEIPL. This ODIN software captures chronologically details of trades including the dealer code/ dealer name.

18. Regarding role of Noticee 1 in Trustline, vide email dated October 18, 2022 (provided as Annexure 1D to the Noticees), Trustline has inter alia stated that the role of Noticee 1 involved complete supervision of all back-end activities and co-ordination including dealing. With respect to dealing, it stated that Noticee 1’s name is mapped to ODIN user ID 29502 since late July, 2021, however, he had been dealing from the said user ID since resignation of another employee, namely, Mr. Sudhakar, in November, 2016. Trustline realized in July, 2021 that the ODIN user name continues to reflect Mr. Sudhakar’s name instead of Noticee 1, after which, they changed the name.

19. Regarding the above, from the trade data submitted by Trustline (provided as Annexure 1C to the Noticees), I note that one Mr. Sudhakar’s name is reflected against ODIN user ID 29502 from July, 2017 onwards, whereas, Noticee 1’s name is reflected from August, 2021 onwards. However, as clarified by Trustline, I note that Noticee 1 was placing orders through the said terminal after resignation of Mr. Sudhakar. Thus, in light of the above, I conclude that Noticee 1 was employed with Trustline before June, 2017. Since he was employed with Trustline before June, 2017 (i.e, during the IP) and punching in orders on its behalf as a dealer, it is reasonable to infer that he had access to non-public information of trades of Trustline.

20. As regards Noticee 3, Trustline vide email dated October 18, 2022, has stated that his role covered office assistance, miscellaneous co-ordination in back-office, KYC checking, following up with banks/ broker for pending works, following up for mail responses from risk team of broker etc. I also note from statement of Noticee 3 recorded on oath before the Investigating Authority, SEBI on August 01, 2022 (provided as Annexure 7A to the Noticees) that in response to question no. 14 whether the information of orders placed or to be placed by Trustline were available with him while trading in his account, his response is recorded as “Yes, I am getting the information through Mr. R. Senthilkumar”. Similarly, in response to question no. 10 and 17, Noticee 1 in his statement recorded on oath before the Investigating Authority, SEBI on August 25, 2022 (provided as Annexure 7B to the Noticees), has inter alia stated that Trustline has taken “Miles” system for allocating funds in the different scrips/different class of assets for each clients which prompts the fund manager, when need arises to allocate funds in different assets class. The fund manager would update the Miles system regarding the quantity of funds to be deployed in a particular asset class and advise the dealer to check the system and place order in the market. Noticee 1 had the credentials for accessing the Miles system and he would get the information of all the impending orders of Trustline, basis which he used to give tips to Mr. Prakash V (Noticee 3). He has further stated that the office premises was small, workstations could be accessed by anyone and there was no restriction on carrying mobile phone.

21. I note that Noticee 1 has pleaded that during investigation, he was enquired in a biased manner and answers were recorded on coercion at the convenience of the Investigation Officer, in such a way as to align statements with that of Noticee 3. Noticee 1 has further stated that his following statements were obtained by coercion:

(i) Noticee 1 was supervising the trading activities of Trustline;

(ii) He had credentials of “Miles System” of Trustline;

(iii) Being the operations manager cum dealer, he was supervising the trading operations and used to get information of impending orders to be placed on behalf of Trustline;

(iv) On the basis of his information about the impending orders of Trustline he used to give tips to Noticee 3;

(v) Based on his tips, Noticee 3 used to trade in scrips from his own trading account as well as from the trading account of Noticee 4;

(vi) Profits earned by Noticee 2 from such trades executed through the trading accounts of Noticees 3 and 4, were shared in the ratio of 50:50 between him (Noticee 1) and Noticee 3.

22. In relation to the above, I have perused the statement of Noticee 1 dated August 25, 2022, I note that the said statement contains the signature of Noticee 1 and further states that

“The statement Is given by me voluntarily without fear, coercion, threat or inducement. This statement is recorded as stated by me and understood by me in proper way before signing. I, R Senthil Kumar also acknowledge that I shall be responsible for the statements and the averments made herein above”. Further, I note that apart from merely claiming that the statement was given by him under coercion, he has not provided any details regarding the kind of coercion, under what circumstances coercion was exercised, any evidence to indicate factual inaccuracy of statement recorded etc. I also note that nearly 8 months after he had given his statement on August 25, 2022, in his first reply dated April 06, 2023, Noticee 1 has claimed coercion, which appears to be an afterthought. I find it relevant here mention decision of Hon’ble Supreme Court in case of Pyare Lal Bhargava vs. State of Rajasthan, AIR1963SC1094, decision dated October 22, 1962, wherein it inter alia held that:

“A retracted confession may form the legal basis of a conviction if the court is satisfied that it was true and was voluntarily made. But it has been held that a court shall not base a conviction on such a confession without corroboration. It is not a rule of law, but is only rule of prudence. It cannot even be laid down as an inflexible rule of practice or prudence that under no circumstances such a conviction can be made without corroboration, for a court may, in a particular case, be convinced of the absolute truth of a confession and prepared to act upon it without corroboration; but is may be laid down as a general rule of practice that it is unsafe to rely upon a confession, much less on a retracted confession, unless the court is satisfied that the retracted confession is true and voluntarily made and has been corroborated in material particulars.”

Importantly, I also note that during the hearing held on April 11, 2023, Noticee 1 submitted that the statement given by him to the Investigating Authority on August 25, 2022 on oath was not given under duress. Thus, in view of Noticee 1’s own admission during hearing and corroborative material available on record such as statement of Noticee 3, trade details of Noticees 2 to 4, WhatsApp chats exchanged between Noticees 1 and 3 etc, I note that retraction of Noticee 1’s statement cannot be regarded as valid and does not alter the conclusions made in this Order.

23. Noticee 1 has argued that Trustline has withheld vital information and that Table 7 only pertains to the year 2022. According to him, the said table does not disclose existence of one Mr. Sathishkumar, (Dealer). Mr Sathish, Mr Ramesh Kumar and Mr Vijayakumar (dealer and co-ordinator) had information about the impending orders and were placing the stocks till 2019. Only after the demise of Mr. Sathish in 2019, Noticee 1 was elevated to the position of operations manager. In this regard, as brought out above, trade data submitted by Trustline read with email dated October 18, 2022 shows that Noticee 1 was placing orders for Trustline from July, 2017 onwards. Thus, submission of Noticee 1 that until 2019, instead of him one Mr. Sathish was placing orders, considering the above submission from Trustline and in absence of evidence to the contrary, does not hold merit.

From the above, I conclude that Noticee 1 who was responsible for operations and dealing in Trustline had knowledge of confidential / non-public information regarding size and timing of impending buy / sell orders of Big Client during the IP.

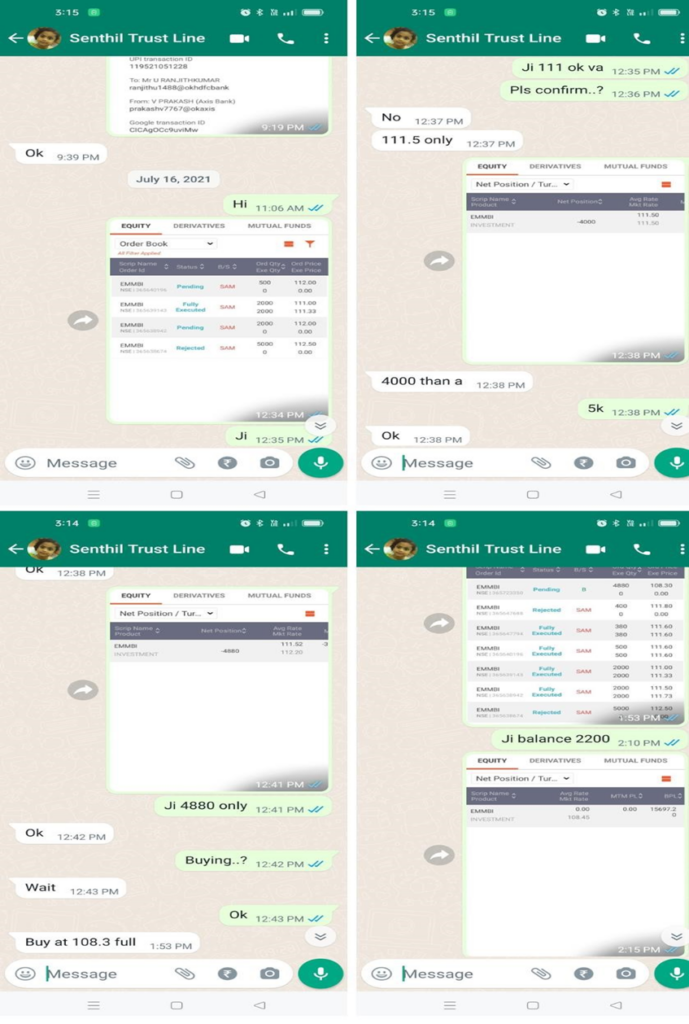

24. With respect to Noticee 3, in his statement, he has inter alia stated that he used to receive information about impending trades of Trustline through Noticee 1. The following extract from WhatsApp chats exchanged between Noticee 1 and 3 is reproduced from Annexure 9 provided to the Noticees:

WhatsApp chat on July 16, 2021

WhatsApp chat on August 23, 2021 between Noticee 1 and Noticee 3[1]

8/23/21, 9:31 AM – 😀😀😀: IMG-20210823-WA0003.jpg (file attached)

8/23/21, 9:31 AM – 😀😀😀: IMG-20210823-WA0004.jpg (file attached)

8/23/21, 10:13 AM – 😀😀😀: IMG-20210823-WA0009.jpg (file attached)

8/23/21, 10:13 AM – 😀😀😀: IMG-20210823-WA0005.jpg (file attached)

8/23/21, 10:13 AM – 😀😀😀: IMG-20210823-WA0007.jpg (file attached)

8/23/21, 10:13 AM – 😀😀😀: IMG-20210823-WA0006.jpg (file attached)

8/23/21, 10:13 AM – 😀😀😀: IMG-20210823-WA0008.jpg (file attached) 8/23/21, 10:13 AM – 😀😀😀: IMG-20210823-WA0010.jpg (file attached)

8/23/21, 12:58 PM – 😀😀😀: Idfc 20000 only

8/23/21, 12:59 PM – 😀😀😀: Sple 4000 only

8/23/21, 1:00 PM – 😀😀😀: pms 500000

8/23/21, 1:00 PM – 😀😀😀: Pms special 135000

25. The above chats suggest that Noticee 3 was actively coordinating with Noticee 1 with respect to the trades he was placing basis information shared by Noticee 1. I note that in the cross-examination held on May 08, 2023 by advocate of Noticee 1, in response to the question “Can one view the contents of the Computer?”, Noticee 3 has responded that

“While one is walking around, one can view the contents of the computer”. Further, when Noticee 3 was specifically asked about the WhatsApp chat that took place on August 23, 2021, he responded that he is unable to identify the said chats. I note that Noticee 3 claimed that he is unable to identify the chats despite the fact that the copy of the said chats obtained by SEBI were provided by Noticee 3 himself vide email dated August 01, 2022. Therefore, Noticee 3’s claim that he could not identify the said chats is clearly contrary to the earlier documented evidence.

26. Noticee 3 has contended that he was merely carrying out instructions for Noticee 1, otherwise it would have cost him his job. However, Noticee 3 has not provided any evidence to support his claim. Further, on perusal of the WhatsApp chats exchanged between him and Noticee 1, and as set out above, where he can be seen initiating conversations with Noticee 1, it does not indicate that Noticee 3 was under any form of duress. No person who is coerced to do something, would willingly initiate the activity he is coerced into. Further, Noticee 3 during the hearing held on April 11, 2023 has admitted that he was not under any pressure from Noticee 1 to execute trades basis tips received of impending orders of Trustline. Therefore, I find it appropriate to reject this contention.

27. Noticee 3 has also contended that he had shared user credentials of demat accounts held by him and his mother with Noticee 1, pursuant to which, Noticee 1 started executing his own research tips in the said trading accounts. In this regard, (i) I note that merely because an individual other than the owner of the account has access to the account does not mean that the said account was solely operated by such individual; (ii) I note that if Noticee 1 had exclusive access to accounts of Noticee 3 and 4, the need for sharing non-public trade information of Big Client on WhatsApp with Noticee 3 as detailed above would not arise; (iii) I note that the trades from account of Noticee 3 were executed from May 02, 2017 to December, 22, 2021 which is before a certain login ID and password was shared by Noticee 3 with Noticee 1 on WhatsApp on June 13, 2022. Further, most of the trades of Noticee 4 were placed between December 13, 2017 to June 20, 2022. For the foregoing reasons, it cannot be conclusively said that Noticee 1 was solely operating the trading account of Noticees 3 and 4. Further, the assertion that Noticee 1 has admitted in his deposition that he alone had login ID and password of Noticee 3’s trading account is borne out of incorrect reading of Noticee 1’s statement. Noticee 1 has admitted that he had login credentials of Miles system which is the software used for allocating funds in different scrips by Trustline and not login credentials of trading account of Noticee 3. Thus, the aforesaid submission of Noticee 3 is not accepted.

ALLEGED FRONT RUNNING TRADES

28. The next question to be determined is whether the orders placed by Noticees 1 and 3, were placed by taking advantage of the non-public information about the impending orders of the Big Client which Noticee 1 and/or Noticee 3 were privy to. The same requires analyzing the particulars of the pattern of trades executed from the trading account of Noticees during the IP.

COMMON SCRIP DAYS AND CHANCES OF BIG CLIENTS’ TRADES MATCHING WITH ALLEGED FRONT RUNNERS

29. In order to analyze the data, it is pertinent to define “Scrip Day”. A combination of a particular trade date and a particular share / scrip is considered as one scrip day. For instance, if a trader trades in six unique scrips in a single day, he is considered as having traded in six scrip days and if these trades were all intra-day, they are considered as six intra-day scrip days. The following is a summary of the trading profiles of the Front Runners i.e., Noticees no. 2 to 4 and the common scrip days they shared with the Big Client, i.e. Trustline:

Table 8

Front Runners | Number of instances for trades executed during the Investigation Period | Common scrip days with Trustline |

|

| % |

Noticee 2 | 1317 | 356 |

|

| 27.03 |

Noticee 3 | 329 | 174 |

|

| 52.89 |

Noticee 4 | 1,335 | 760 |

|

| 56.93 |

30. From the above table, it is observed that there is a significant overlap in the scrip days between the trading activities of the Noticees and the Big Client. Regarding the above, Noticee 1 has contended that 27% of total order match by Noticee 2 is purely coincidental while orders of Noticees 3 and 4 matched to an extent of 52 to 57%. In this regard, I find that in a universe of numerous securities/derivative contracts being traded on stock exchange platform, it is surprising to observe that the trades executed from the trading accounts of Noticees are found to be in the same scrip on the same day as that of the Big Client on a regular basis amounting to 27% and extending upto 56.93%. Thus, I do not agree that 27% of common scrip days as Big Client can be considered as coincidental.

In addition, several trades of Noticees 2-4 exhibit the tell-tale Buy-Buy-Sell and Sell-SellBuy patterns typical of front-running operations, as we shall elaborate below.

31. Before proceeding to discuss the pattern followed in front running instances, I find it relevant to discuss the strategies commonly used to front run trades. In Buy-Buy-Sell (BBS) trading pattern, the alleged front runner, by using the non-public information regarding an impending buy order of the big client, places his buy order before the big client’s buy order. As and when the big client places a buy order, the price of the security rises and the alleged front runner sells the securities bought earlier, at the raised price, thereby pocketing the difference between the new raised price of the security which is established during / post big client’s buy trades and the price at which he had bought his securities. Further, in the Sell-Sell-Buy (SSB) trading pattern, the alleged front runner by using the non-public information regarding an impending sell order of the big client, places his sell orders before the big client’s sell order. When the big client places a sell order, the price of the security falls which gives an opportunity to the alleged front runner to buy back the securities at a lower price to meet his obligations which he had created earlier by selling securities.

32. In the present case, following the pattern illustrated above, the orders have been orchestrated in such a manner that the trades executed follow a sequence – buy trade of the front runner, buy trade of the Big Client either before or coinciding with the sell trade of the front runner or sell trade of the front runner, sell trade of the Big Client either before or coinciding with the buy trade of the front runner. In other words, the trading pattern of Noticees 2 to 4 appears to be, firstly taking the same position as that of the impending Big Client order and then squaring off the position when the Big Client places its order. Further, the timing and price of placing such limit orders of the alleged front runners and the Big Client are in such a manner that the trades of the alleged front runners match with the trades of the Big Client.

FRONT RUNNING INSTANCES

33. The period during which the front runners had traded and the no. of scrips in which trades were executed are given below:

Table 9

# | Noticee | Period | No. of scrips |

1. | Geetha N. (Noticee 2) | August 11, 2017 to June 20, 2022 | 46 |

2. | Prakash V. (Noticee 3) | May 02, 2017 to December 22, 2021 | 38 |

3. | Geetha V. (Noticee 4) | December 13, 2017 to June 20, 2022 | 83 |

To demonstrate the pattern of the front running instances, order placement analysis of account of Noticees 2 to 4 was undertaken for sample scrip days. Few illustrative instances of such activity are as follows:

Geetha N (Noticee 2)

34. The material available on record shows that in 233 instances of trades of Noticee 2, BBS pattern was observed whereas in 30 instances, SSB pattern was observed. A sample instance of each pattern is given as under:

Table 10: BBS Pattern

Trade date | Symbol | Big client activity | Big order buy qty | Big order sell qty | FR buy qty | FR sell qty | Matchi ng % | Buy order time by FR | Buy order time by Big Client | Sell order time by FR | Square d off diff (Rs.) |

06/02/2020 | EMMBI | Buy | 4,969 | 0 | 1,000 | 1,000 | 100.00 | 1:36:42 PM | 2:12:25 PM to 2:16:15 PM | 2:54:4 2 PM

| 2,635.55 |

35. From the above, it can be seen that on February 06, 2020, a buy order for 1,000 shares of EMMBI Industries Limited (“EMMBI”), was placed from the trading account of Noticee 2 at 01:36:42 PM i.e., just prior to the impending buy order of the Big Client for 4,969 shares of EMMBI, placed between 02:12:25 PM and 02:16:15 PM. Subsequently as soon as the large buy order of Trustline was placed, a sell order in the scrip of EMMBI was placed for 1,000 shares at 02:54:42 PM in the trading account of Noticee 2 so as to square off the earlier buy position of 1,000 shares. Such BBS front running pattern resulted into a profit of Rs. 2,635.55 for Noticee 2 and also 100% of the quantity of the sell order of Noticee 2 got matched with buy orders of the Big Client in the aforementioned illustration.

Table 11: SSB pattern

Trade date | Symbol | Big client activity | Big order buy qty | Big order sell qty | FR buy qty | FR sell qty | Matching % | Sell order time by FR | Sell order time by Big Client | Buy order time by FR | Squared off diff (Rs.) |

20/04/2021 | KDDL | Sell | – | 20,100 | 300 | 300 | 100.00 | 1:07:33 PM

| 1:18:05 PM to 3:02:02 PM | 2:23:12 PM

| 6,018.15 |

36. From the table above, it can be seen that on April 20, 2021, a sell order for 300 shares of KDDL was placed from the trading account of Noticee 2 at 01:07:33 PM e., prior to the impending sell orders of the Big Client were placed for 20,100 shares of KDDL, between 01:18:05 PM and 03:02:02 PM. Subsequently, a buy order in the scrip of KDDL was placed for 300 shares at 14:23:12 from the trading account of Noticee 2 to square off the sell trades for 300 shares. Such SSB front running pattern in the scrip of KDDL resulted into a profit of Rs 6,018.15 for Noticee 2. Further, 100% of the quantity of the buy order of Noticee 2 matched with sell orders of the Big Client in the aforementioned illustration. The aggregate of profits so earned upon squaring off all such trades executed from the trading account of Noticee 2 in respect of the 233 BBS instances and 30 SSB instances as observed in the course of investigation, amounted to Rs 12,10,234.

37. Noticee 1 has argued that the allegation of front running basis trades executed from account of Noticee 2 by Noticee 1 following a BBS and/or SSB pattern around the timing of placement of orders of the Big Client as detailed in paragraphs 43 to 48 of the Interim Order, is merely on the basis of surmises and false statement of Noticee 3. I find that Noticee 1 has not explained how trade data amounts to “surmises”. Trade data submitted by the exchanges to SEBI is objective information. Instances of front running found are based on objective assessment of this trade data and not solely based on statement of Noticee 1 or 3 or any other individual. Thus, I find it appropriate to preliminarily reject this argument.

38. Noticee 2 has submitted that all trades in her account were executed by Noticee 1 and that she did not have knowledge or intention to front run the trades of Trustline. I find that the aforesaid submission is strengthened by the fact that Noticee 1 by affidavit dated September 13, 2022 has admitted that he had opened Noticee 2’s trading account and carried out trading through the said account. In this regard, I find it appropriate to mention here the order passed by Hon’ble SAT in Mahavirsingh N Chauhan and Anr. vs. SEBI (Appeal No. 393 of 2018) decided on October 18, 2019, wherein Hon’ble SAT held that:

“We are of the opinion that by renting their demat account, trading account etc., the appellants were concealing the identity of the fraudster and, thus, were acting not only in concert but in connivance with the said fraudster. The appellants cannot, thus, escape from the liability of debarment and the wrongful gains made by them.” Even though the aforesaid order concerns renting of demat account, whereas in the present case, it cannot be strictly said that Noticee 2 had rented her trading account to Noticee 1 in absence of consideration, it does however highlight that when a registered owner of an account lets another person use his/her account which is ultimately used for fraudulent activities, the registered owner cannot be allowed to evade his/her responsibility for his/her omission to act in a prudent manner. It is pertinent to note that the wrongful gains have been made with the help of Noticee 2, i.e, if not for her co-operation in letting her account be used by Noticee 1, unlawful gains in her account would not been made, hence, not holding her liable for the unlawful gain, will leave room for violators who are the brains behind the scheme to unjustly enrich their accomplices and then claim exemption for such accomplices citing that such accomplices had no knowledge or intention or had given control of their account to the violators. Especially in light of the fact that it has not come on record how the unlawful gains made in accounts of Noticees were utilised (apart from the fact that gains made in accounts of Noticees 3 and 4 were distributed in 50:50 ratio between Noticees 1 and 3), Noticee 2 who participated in the fraud, cannot be absolved of her liability merely because she was unaware regarding the trades executed from her account.

Prakash V (Noticee 3)

39. The material available on record shows that in 124 instances of trades of Noticee 3, BBS pattern was observed whereas in 21 instances, SSB pattern was observed. A sample instance of each pattern is given as under:

Table 12: BBS pattern

Trade date | Scrip Symbol | Trustline activity | Trustline buy qty | Noticee 3 buy qty | Noticee 3 sell qty | Matching % | Buy order time by FR | Buy order time by Big Client | Sell order time by FR | Profit earned by Noticee 3 (INR) |

11/02/2021 | ENIL | Buy | 67,284 | 2,520 | 2,520 | 100.00 | 12:13:10 PM To 12:28:59 PM

| 12:25:46 PM 2:55:51 PM

| 1:02:11 PM

| 18,356.35 |

40. From the above, it can be seen that on February 11, 2021, buy orders for 2,520 shares of Entertainment Network (India) Ltd. (“ENIL”) were placed by Noticee 3 between 12:13:10 PM and 12:28:59 PM i.e., prior to the impending buy orders of the Big Client for 67,284 securities of ENIL, placed between 12:25:46 PM and 02:55:51 PM. Subsequently, a sell order in the scrip of ENIL was placed for 2,520 securities at 01:02:11 PM by Noticee 3 to square off the earlier position taken for 2,520 securities. Such BBS front running pattern resulted into a profit of Rs. 18,356.35 for Noticee 3. Further, 100% of the quantity of the sell order of Noticee 3 matched with buy orders of the Big Client in the aforementioned illustration.

Table 13: SSB pattern

Trade date | Scrip Symbol | Trustline activity | Trustline sell qty | Noticee 3 buy qty | Noticee 3 sell qty | Matching % | Sell order time by FR | Sell order time by Big Client | Buy order time by FR | Profit earned by Noticee 3 (INR) |

13/01/2021 | HMVL | Sell | 80,199 | 4,550 | 4,550 | 100.00 | 11:12:32 AM to 11:30:27 AM

| 11:20:49 AM to 2:35:15 PM

| 1:03:43 PM

| 8,616.05 |

41. From the table above, it can be seen that on January 13, 2021, sell orders for 4,550 shares of Hindustan Media Ventures Limited (“HMVL”) were placed from the trading account of Noticee 3 between 11:12:32 AM and 11:30:27 AM i.e., prior to the impending sell orders of the Big Client for 80,199 shares of HMVL, placed between 11:20:49 AM and 02:35:15 PM. Subsequently, a buy order in the scrip of HMVL was placed for 4,550 shares at 01:03:43 PM by Noticee 3 from his trading account to square off his sell position taken earlier for 4,550 shares. Such SSB front running pattern in the scrip of HMVL resulted into a profit of Rs. 8616.05 for Noticee 3. Further, 100% of the quantity of the buy order of Noticee 3 matched with sell orders of the Big Client in the aforementioned illustration. It is seen that the cumulative gains earned by way of the difference upon squaring off all such trades by Noticee 3 executed from his trading account as observed above, amounted to Rs. 5,40,196.

42. Noticee 3 has contended that in 2014, Noticees 1 and 3 were colleagues in Trustline. In 2015, Noticee 1 started his own started his own sub-brokerage firm registered with Angel Broking Ltd. (now Angel One). In 2016, he collected Rs. 1,40,000 from Noticee 3, promising to generate good returns. After few months, Noticee 1 declared that the money Noticee 3 had given to him was lost. After rejoining Trustline in 2016-2017, Noticee 1 gave a guarantee to recover the loss incurred with Noticee 3’s money by providing him with research tips (stock buy and sell recommendations). As per Noticee 3, Noticee 1 stated that he would be charging commission for the stock tips he was providing Noticee 3, since the recommendations were based on his own research, and he was also charging similar fees to a few other clients he was handling at the time. I find that even if submission of Noticee 3 were to be accepted, it does not justify using non-public trade information of Trustline to execute trades. Noticee 1 and/or Noticee 3 have not demonstrated how the information shared by Noticee 1 was based on his own research. Thus, this submission does not hold any merit.

43. Noticee 3 has provided certain images of trading strategy, candlestick patterns, bearing chart pattern, bullish chart pattern etc to demonstrate that Noticee 1 was carrying out his own research for creating stock tips for Noticee 3. However, I find that merely based on some isolated images, it cannot be said that Noticee 1 was conducting his own research when compared to the overwhelming evidence brought on record that Noticee 1 was infact using non-public trade information of Trustline. Thus, this submission does not hold any weight.

Geetha V (Noticee 4)

44. The material available on record shows that in 518 instances of trades of Noticee 4, BBS pattern was observed, whereas in 86 instances, SSB pattern was observed. A sample instance of each pattern is given as under:

Table 14: BBS pattern

Trade date | Scrip symbol | Big Client activity | Big Client buy qty | Noticee 4 buy qty | Noticee 4 sell qty | Matching % | Buy order time by FR | Buy order time by Big Client | Sell order time by FR | Profit earned by Noticee 4 (INR) |

28/01/2021 | ENIL | Buy | 1,10,000 | 10,000 | 10,000 | 75 | 12:44:51 PM to 2:09:37 PM

| 12:52:53 PM To 3:03:42 PM

| 2:11:24 PM To 2:11:49 PM

| 1,02,636.45 |

45. From the table above, it can be seen that on January 28, 2021, buy orders for 10,000 securities of ENIL were placed from the trading account of Noticee 4 between 12:44:51 PM and 02:09:37 PM i.e., prior to the impending buy orders of the Big Client for 1,10,000 securities of ENIL, placed between 12:52:53 PM and 03:03:42 PM. Subsequently, sell orders in the scrip of ENIL were placed for 10,000 securities from 02:11:24 PM and 02:11:49 PM from the trading account of Noticee 4 to square off the earlier buy position taken for 10,000 securities. The above noted BBS front running pattern resulted into earning of a profit of Rs. 102,636.45 in the account of Noticee 4. 75% of the quantity of the sell order of Noticee 4 in ENIL matched with buy orders of the Big Client as noted in the aforementioned illustration.

Table 15: SSB pattern

Trade date | Scrip Symbol | Big Client activity | Big Client sell qty | Noticee 4 buy qty | Noticee 4 sell qty | Matching % | Sell order time by FR | Sell order time by Big Client | Buy order time by FR | Profit earned by Noticee 4 (INR) |

26/04/2022 | KDDL | Sell | 6,600 | 245 | 245 | 92 | 12:16:58 PM to 3:06:36 PM

| 12:59:02 PM to 3:24:59 PM

| 1:20:30 PM to 3:07:03 PM

| 6,229.25 |

46. From the above, it can be seen that on April 26, 2022, sell orders for 245 shares of KDDL Limited (“KDDL”) were placed from account of Noticee 4 between 12:16:58 PM to 3:06:36 PM prior to the impending sell orders of Big Client for 6600 shares of KDDL placed between 12:59:02 PM to 3:24:59 PM. Subsequently, buy orders in scrip of KDDL were placed for 245 shares by Noticee 4 from 1:20:30 PM to 3:07:03 PM to square off the earlier sell position taken for 245 shares. Such SSB front running pattern in the scrip of KDDL resulted into a profit of Rs. 6,229.25 for Noticee 4. Further, 92% of the quantity of the buy order of Noticee 4 matched with sell orders of the Big Client in the aforementioned illustration. The cumulative and aggregated difference upon squaring off all such trades executed from the trading account of Noticee 4 amounted to Rs 40,15,791.

47. The trading pattern in accounts of Noticees 2 to 4 above shows that the first leg of trades was placed/executed just prior to the impending orders of Trustline and the second leg of the intra-day trade (squaring off trades) were placed prior to the last tranche of order by Trustline or immediately after it resulted into a profit. The aforesaid pattern coupled with the fact that Noticees 1 and 3 had access to non-public trade information of Trustline, statements of Noticees 1 and 3, and trades of Noticees 2 to 4 during the IP leads to a preponderance of probability that Noticees took advantage of the non-public information of impending trades of Trustline to front run its trades. The trades in accounts of Noticees 2 to 4 appearing to front run the trades of Trustline were provided as Annexures 4 to 6 to the Noticees.

WHATSAPP CHATS, CORRESPONDING TRADES AND TRANSFER OF PROFIT MADE BETWEEN NOTICEES 1 AND 3

48. Illustrative WhatsApp chat exchanged between Noticees 1 and 3 (provided as Annexure 9 to the Noticees), trades corresponding to the said chats (provided as Annexure 4, 5 and 6 to the Noticees) and the profit made pursuant to the above are discussed herein.

WhatsApp chat on August 06, 2021

8/6/21, 10:59 AM – 😀😀😀: Hi ji

8/6/21, 11:32 AM – Senthil Trust Line: No ji

8/6/21, 11:49 AM – Senthil Trust Line: Buy jash 1000 at 570 disclose

8/6/21, 11:51 AM – Senthil Trust Line: Modify to 567

8/6/21, 11:53 AM – Senthil Trust Line: Buy between 567 to 570

8/6/21, 11:53 AM – Senthil Trust Line: Pottu edu