CIRCULAR

SEBI/HO/IMD/DF3/CIR/P/2018/04 January 4, 2018

All Mutual Funds/Asset Management Companies /

Trustee Companies/Boards of Trustees of Mutual Funds/ AMFI

Sir/ Madam,

Subject: Benchmarking of Scheme’s performance to Total Return Index

- Mutual Funds are required to disclose the name(s) of benchmark index/indices with which the AMC and trustees would compare the performance of the scheme in scheme related documents.

- At present, most of the mutual fund schemes (other than debt schemes) are benchmarked to the Price Return variant of an Index (PRI). PRI only captures capital gains of the index constituents. On the other hand, Total Return variant of an Index (TRI) takes into account all dividends/ interest payments that are generated from the basket of constituents that make up the index in addition to the capital gains. Hence, TRI is more appropriate as a benchmark to compare the performance of mutual fund schemes.

- With an objective to enable the investors to compare the performance of a scheme visà-vis an appropriate benchmark, it has been decided that:

(a) Selection of a benchmark for the scheme of a mutual fund shall be in alignment with the investment objective, asset allocation pattern and investment strategy of the scheme.

(b) The performance of the schemes of a mutual fund shall be benchmarked to the Total Return variant of the Index chosen as a benchmark as stated in para (a) above.

(c) (i) Mutual funds shall use a composite CAGR figure of the performance of the PRI benchmark (till the date from which TRI is available) and the TRI (subsequently) to compare the performance of their scheme in case TRI is not available for that particular period(s).

(ii) The calculation of composite CAGR is elaborated with an example in the following paragraph.

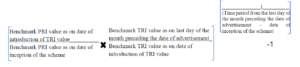

For instance, ABC scheme had been launched on August 2, 1995. The benchmark PRI values are available from the date of inception of the fund. The benchmark TRI values are available from June 30, 1999. The calculation of a composite benchmark performance return in CAGR terms would be as given below:

The aforesaid is explained with an example:

Example: Consolidated Benchmark CAGR (PRI and TRI) | ||

Date | Benchmark PRI values | Benchmark TRI values |

02/08/1995 | 1007.57 |

|

30/06/1999 | 1187.70 | 1256.38 |

30/11/2017 | 10226.55 | 13966.58 |

CAGR | 12.20% | |

Thus, in the above example (for advertisements in the month of December, 2017 the last of the preceding month would be November 30, 2017),

CAGR= [(1187.70/1007.57)*(13966.58/1256.38) ^ (1/22.3452)]-1

[1 year= 365 days]

CAGR= 12.20%

(iii) Mutual funds shall use the composite CAGR as explained above, subject to making the following disclosure:

*As TRI data is not available since inception of the scheme, benchmark performance is calculated using composite CAGR of XYZ (name of the benchmark index) PRI values from date…. to date… and TRI values since date….”

4. This circular is applicable to all schemes of Mutual Funds with effect from February 1, 2018.

This circular is issued in exercise of the powers conferred under Section 11 (1) of the Securities and Exchange Board of India Act, 1992, read with the provision of Regulation 77 of SEBI (Mutual Funds) Regulations, 1996 to protect the interests of investors in securities and to promote the development of, and to regulate the securities market.

Yours faithfully,

DEENA VENU SARANGADHARAN

Deputy General Manager

Tel no.: 022-26449266

Email: [email protected]

{kind=link}