BEFORE THE ADJUDICATING OFFICER

SECURITIES AND EXCHANGE BOARD OF INDIA

[ADJUDICATION ORDER NO. Order/BM/DS/2024-25/30906]

UNDER SECTION 15-I OF THE SECURITIES AND EXCHANGE BOARD OF INDIA ACT, 1992 READ WITH RULE 5 OF SEBI (PROCEDURE FOR HOLDING INQUIRY AND IMPOSING PENALTIES) RULES, 1995

IN THE MATTER OF

Mr Arun N

PAN No.: ARHPA4708R

SEBI RA Regn No.: INH200007353

FACTS OF THE CASE

1. Securities and Exchange Board of India (hereinafter referred to as “SEBI”) conducted inspection of Mr Arun N, Research Analyst (hereinafter referred to as “Noticee”) on March 05, 2024 and March 07, 2024 to look into various compliance requirements adhered by the Noticee with respect to the provisions of SEBI (Research Analysts) Regulations, 2014 (hereinafter referred to as “RA Regulations, 2014”) and applicable SEBI Circulars. The period covered in inspection was from April 01, 2022 to February 29, 2024 (hereinafter referred to as “inspection period” / “IP”). Noticee is registered as research analyst with SEBI registration no. INH200007353.

2. The findings/ observations made during the course of inspection were communicated to the Noticee by SEBI vide letter dated March 21, 2024. After examining the reply submitted by the Noticee vide emails dated April 03, 2024, April 04, 2024, April 08, 2024, and April 16, 2024, it was alleged that the Noticee violated various provisions of RA Regulations, 2014, SEBI (Prohibition of Fraudulent and Unfair Trade Practices relating to Securities Market) Regulations, 2003 (hereinafter referred to as “SEBI PFUTP Regulations, 2003”) and applicable SEBI Circulars. The extracts of violations alleged to have been committed by the Noticee and the corresponding provisions of RA Regulations, 2014, SEBI PFUTP Regulations, 2003 and SEBI Circulars are given in the tabulation below:

Table 1

|

|

3. SEBI initiated adjudication proceedings against the Noticee under Section 15EB and Section 15HA of the SEBI Act, 1992 for the alleged violations of the relevant provisions as stated above.

APPOINTMENT OF ADJUDICATING OFFICER

4. The undersigned was appointed as the Adjudicating Officer (AO) vide Order dated July 03, 2024 under Section 15-I of the SEBI Act, 1992 and Rule 3 of SEBI (Procedure for Holding Inquiry and Imposing Penalties) Rules, 1995 (hereinafter referred to as “SEBI Adjudication Rules”), to inquire into and adjudge under Section 15EB and Section 15HA of the SEBI Act, 1992, the violations of aforesaid provisions alleged to have been committed by the Noticee.

SHOW CAUSE NOTICE, REPLY OF THE NOTICEE AND HEARING

5. Show Cause Notice No. SEBI/EAD/BM/DS/26013/1/2024 dated August 14, 2024 (hereinafter referred to as “SCN”) was issued to the Noticee in terms of Section 15-I of the SEBI Act, 1992 and rule 4 of SEBI Adjudication Rules, to show cause as to why an inquiry should not be held against it and why penalty, if any, under Section 15EB and Section 15HA of the SEBI Act, 1992 be not imposed on the Noticee.

6. The SCN was duly served on the Noticee through SPAD and digitally signed email. Vide letter dated September 14, 2024, the Noticee submitted its replies.

7. The submissions made by the Noticee are as summarized below:

Outsourcing of KYC Activities

- Noticee is in full compliance of KYC norms today. He has appointed CVLKRA. The details of significant number of customers were collected by the Noticee, and the process was not outsourced. Noticee has provided link of the KYC documents of the clients collected by him, in support of his submissions that he was collecting the documents.

- Delay in obtaining KYC documents of clients was due to the clientele being acquired during covid period, with limited retention of these clients.

- GAP-UP operates as an aggregator platform, enabling individuals to select Board-registered Research Analysts based on their preferences. The platform’s maintenance involves significant technical challenges and the provision of seamless payment services, which are both cost-intensive. Consequently, Research Analysts utilize GAP-UP for backend support, including payment and billing systems, as well as profile management. The business model of GAP-UP entails collecting all payments under its own name, deducting its service charges, and subsequently distributing the remaining funds to the Research Analysts. GAP-UP charges a percentage of the income generated through its platform for billing and content hosting services, and remits the remainder to the Research Analyst’s account.

- The Noticee provided a copy of the email that provides evidence of GAP-UP’s collection of platform fees. Specifically, the email details a 50% fee for the initial purchase of his content and a 10% fee for any subsequent subscription renewals. The said platform fees are for hosting of the domain and the content and billing services – which is once again evidenced by the various invoices raised by GAP-UP. Thus, there is no agreement of any kind for any service with GAP-UP for collection of KYCs. Further, there is no document / evidence to suggest that the Noticee had outsourced KYC to Gap-Up or any other third party.

Offering assured returns

- ‘75% accuracy’ refers to the timing in which the calls are made and not anything else. Noticee has never provided any promises or guarantees of assured or risk-free returns to his clients at any time. Noticee has consistently taken steps to ensure that clients are fully aware that investments inherently carry risks and that there is no guarantee of a fixed income or return.

- A holistic reading of the selected messages would provide a background and the context in which they were sent and would evince a different meaning. Further, as a means to avoid any doubts, Noticee has taken steps to pull down such messages and is duly disseminating information in consonance with the Regulations and educating clients.

- Regulation 4 of PFUTP Regulations, 2003 shall not be applicable in the instant case as the Noticee has never done any act that amounts to diversion, misutilisation or siphoning off of assets or earnings of a company or any device, scheme or artifice to manipulate the books of accounts or financial statement of such a company that would directly or indirectly manipulate the price of securities of that company or has he engaged in transactions through mule accounts.

- All the acts of the Noticee are streamlined and are in due compliance of the SEBI (Research Analysts) Regulations, 2014 and the SEBI Circular on Advertisement code for Investment Advisers and Research Analysts. The wholesome reading of the selected messages would show that there has not been any promise or guarantee of assured or risk-free return to the investors. To erase all doubts, Noticee has taken all necessary steps to pull down any such messages and all his communications are in strict compliance with the Regulations.

8. Vide letter dated September 17, 2024, hearing notice was issued to Noticee to provide opportunity of personal hearing in the interest of natural justice. The Noticee was advised to appear for the hearing before the undersigned on October 16, 2024. Vide email dated October 14, 2024, the Noticee requested for rescheduling of the hearing. The Noticee’s request was accepted. Vide email dated October 15, 2024, the Noticee was advised to appear for the hearing on October 22, 2024. The Noticee appeared for the scheduled hearing through its authorized representative (AR). The AR reiterated submission made vide letter dated September 14, 2024. The AR requested time till October 23, 2024 to submit a summary of his letter dated September 14, 2024. The request was acceded to. The Noticee submitted the summary vide email dated October 23, 2024.

CONSIDERATION OF ISSUES AND FINDINGS

9. Considering the allegations made out in the SCN and the submissions made by the Noticee, the following issues require consideration in the present case:

ISSUE I – Whether the Noticee is in violation of the provisions of RA Regulations, 2014, SEBI PFUTP Regulations, 2003 and applicable SEBI Circulars, as given in Table 1 above?

ISSUE II – Do the violations, if any, attract penalty under section 15EB and section HA of the SEBI Act, 1992?

ISSUE III – If so, what would be the monetary penalty that can be imposed taking into consideration the factors mentioned in Section 15J of SEBI Act, 1992?

10. The said provisions under which violations have been alleged against the Noticee are reproduced below –

SEBI Act, 1992

Prohibition of manipulative and deceptive devices, insider trading and substantial acquisition of securities or control.

12A. No person shall directly or indirectly—

- use or employ, in connection with the issue, purchase or sale of any securities listed or proposed to be listed on a recognized stock exchange, any manipulative or deceptive device or contrivance in contravention of the provisions of this Act or the rules or the regulations made thereunder;

- employ any device, scheme or artifice to defraud in connection with issue or dealing in securities which are listed or proposed to be listed on a recognised stock exchange;

- engage in any act, practice, course of business which operates or would operate as fraud or deceit upon any person, in connection with the issue, dealing in securities which are listed or proposed to be listed on a recognised stock exchange, in contravention of the provisions of this Act or the rules or the regulations made thereunder;

SEBI (Prohibition of Fraudulent and Unfair Trade Practices relating to Securities Market) Regulations, 2003

4. Prohibition of manipulative, fraudulent and unfair trade practices

(1) Without prejudice to the provisions of regulation 3, no person shall indulge in a manipulative, fraudulent or an unfair trade practice in securities markets. 1[Explanation.-For the removal of doubts, it is clarified that-

- any act of diversion, misutilisation or siphoning off of assets or earnings of a company whose securities are listed or any concealment of such act or any device, scheme or artifice to manipulate the books of accounts or financial statement of such a company that would directly or indirectly manipulate the price of securities of that company, or

- transactions through mule accounts for indulging in manipulative, fraudulent and unfair trade practice shall be and shall always be deemed to have been included in sub-regulation (1).]

SEBI (Research Analysts) Regulations, 2014

General responsibility.

1 Substituted vide the Securities and Exchange Board of India (Prohibition of Fraudulent and Unfair Trade Practices relating to Securities Market) (Amendment) Regulations, 2024 w.e.f. July 1, 2024. Before the substitution, the Explanation read as follows:

“Explanation.-For the removal of doubts, it is clarified that any act of diversion, misutilisation or siphoning off of assets or earnings of a company whose securities are listed or any concealment of such act or any device, scheme or artifice to manipulate the books of accounts or financial statement of such a company that would directly or indirectly manipulate the price of securities of that company shall be and shall always be deemed to have been considered as manipulative, fraudulent and an unfair trade practice in the securities market. ”

(1) …

(2) Research analyst or research entity shall abide by Code of Conduct as specified in Third Schedule.

Third Schedule – Code Of Conduct For Research Analyst

- Honesty and Good Faith – Research analyst or research entity shall act honestly and in good faith.

- Diligence – Research analyst or research entity shall act with due skill, care and diligence and shall ensure that the research report is prepared after thorough analysis.

- Compliance – Research analyst or research entity shall comply with all regulatory requirements applicable to the conduct of its business activities.

- Responsibility of senior management – The senior management of research analyst or research entity shall bear primary responsibility for ensuring the maintenance of appropriate standards of conduct and adherence to proper procedures.

SEBI Circular No.: SEBI/HO/MIRSD/ MIRSD-PoD-2/P/CIR/2023/51 dated April 05, 2023 – Advertisement code for Investment Advisers (IA) and Research Analysts (RA)

- Securities and Exchange Board of India (Investment Advisers) Regulations, 2013 and Securities and Exchange Board of India (Research Analysts) Regulations, 2014 provide for code of conduct to be followed by IAs and RAs respectively. In order to further strengthen the conduct of IAs and RAs, while issuing any advertisement, it is directed that IAs/RAs shall ensure compliance with the advertisement code as prescribed below:

- .

- .

4. Prohibitions in the advertisement:

The advertisement shall not contain:

1. Any promise or guarantee of assured or risk free return to the investors. The advertisement shall not imply any assured returns or minimum returns or target return or percentage accuracy or service provision till achievement of target returns or any other nomenclature that gives the impression to the client that the investment advice/recommendation of research report is risk-free and/or not susceptible to market risks and/or that it can generate returns with any level of assurance.

xii. Reference to past performance of the IA/RA.

SEBI Circular No. SEBI/HO/MIRSD-PoD-2/P/CIR/2023/90 dated June 15, 2023 Master Circular for Research Analysts

9. Guidelines on Outsourcing of Activities by Intermediaries 9.1 …

9.5 Activities that shall not be Outsourced:

a. The intermediaries desirous of outsourcing their activities shall not, however, outsource their core business activities and compliance functions. An example of core business activity may be – execution of orders and monitoring of trading activities of clients in case of stock brokers. Regarding Know Your Client (KYC) requirements, the intermediaries shall comply with the provisions of SEBI {KYC (Know Your Client) Registration Agency} Regulations, 2011 and Guidelines issued thereunder from time to time.

11. The findings in each of the alleged violations against the Noticee in the SCN dated August 14, 2024 are given below.

12. Outsourcing of KYC Activities-

12.1 It was observed that the Noticee had commenced giving stock recommendation through Gap up from September 2023. As on March 05, 2024, the Noticee had 390 clients enrolled through this arrangement, as per the subscription details submitted by the Noticee vide email dated April 08, 2024.

12.2 Gap-up website hosts around 30-40 SEBI registered RAs in its website and provides highlights about the SEBI registered RAs with whom it has tie-ups. The clients can choose the RA of their liking, based on the videos posted in the website and can join the free telegram channel provided by Gap-up wherein all the RAs give free recommendation and clients can subscribe to the paid Telegram channel of the respective RA by paying the subscription fees. The clients also pay through the website of GAP-up. Once payment is confirmed, the client will be added to the paid telegram channel of the respective RA. The revenue sharing between the RA and Gap-up is in the ratio given in the table below.

Type | User 1st purchase | User -Renewal | ||

Creater Cut% | Marketing Cut% | Creater Cut% | Marketing Cut% | |

Gap-up website | 50% | 50% | 90% | 10% |

Gap-up telegram | 20% | 80% | 20% | 80% |

|

12.3 Since the clients were on boarded through the website of Gap-up and Telegram channel, the Noticee was not having KYC of the clients. He was only in possession of the name, mobile number and email id provided by the clients. Thus, no verification of the client records was carried out by him. The Noticee had informed during the inspection that that he was not carrying out KYC of its clients, he has only name, mobile no. and email id available with him.

12.4 As per the provisions of Clause 9.5 of master circular for RA SEBI/HO/MIRSD- PoD-2/P/CIR/2023/90 dated June 15, 2023, a research analyst shall not outsource their core activities and compliance functions. Regarding KYC requirements, it shall comply with the provisions of SEBI {KYC (Know Your Client) Registration Agency} Regulations, 2011 and Guidelines issued thereunder. As per the provisions of clauses 1,2, 7 & 8 of the Code of Conduct as specified in Third Schedule under Regulation 24 (2) of the SEBI RA Regulations, 2014, a research analyst shall act honestly and in good faith; shall act with due skill, care and diligence; shall comply with all regulatory requirements applicable to the conduct of its business activities; and shall maintain appropriate standards of conduct and adherence to proper procedures.

12.5 In this regard, the Noticee, vide email dated April 08, 2024, inter-alia submitted that he could not obtain KYC of certain clients on account of the difficulties/ technical issues faced at the time of Covid. He has initiated process for registering with CAMS for KYC compliance in future on boarding of clients. It had also submitted a copy of the email sent to CAMS on April 01,2024.

12.6 Thus, it was observed that the Noticee has not done KYC of his clients during the inspection period, and has outsourced KYC and client on-boarding activities. In view of the same, it was alleged that the Noticee has violated the provisions of Clause 9.5 of master circular for RA SEBI/HO/MIRSD-PoD- 2/P/CIR/2023/90 dated June 15, 2023 read with clauses 1,2, 7 & 8 of the Code of Conduct as specified in Third Schedule under Regulation 24 (2) of the SEBI RA Regulations, 2014.

12.7 The Noticee has submitted that he has never outsourced its KYC activities to Gap-up or any other entity. He admitted that he was not in possession of all KYC documents of his clients at the time of inspection. He further submitted that Gap-up was just an aggregator, which provided interface to the Noticee and various other RAs to acquire clients. Gap-up functions as a marketplace for the RAs, and also provides billing services and displays profiles of the RAs, but does not participate into any of the functions of the RA, including KYC activities. Noticee has also submitted that it had subsequently registered himself with CVLKRA for KYC.

12.8 It is noted that the Noticee had not completed KYC for all his clients at the time of inspection. It is further noted that he was acquiring clients through Gap-up website, and sharing revenue as per his agreement with Gap-up. During the inspection, the Noticee had informed that he was not carrying out KYC of its clients, and that he had only name, mobile no. and email id available with him. Further, he was able to provide KYC documents of 38 clients out of the 390 clients onboarded through Gap-up website.

12.9 In view of the aforesaid, it is observed that the Noticee was not conducting KYC of his clients during the inspection period and was relying on the Gap-up website for the onboarding and KYC of the clients. Thus, he was outsourcing the KYC activities of his clients to the Gap-up website. The Noticee has submitted that he has registered with CVLKRA for the KYC of his clients subsequent to the inspection. However, during the inspection period, the Noticee was relying on the Gap-up website for the client KYC details and thus was outsourcing the KYC activities. Being a SEBI registered Research Analyst, it was Noticee’s responsibility to complete KYC of all his clients. However, he has not fulfilled his responsibility, and has not acted with due skill, care and diligence, by not complying with the provisions of the RA Regulations, 2014 and applicable SEBI Circular. Therefore, the allegation of violation of provisions of Clause 9.5 of Master Circular for RA SEBI/HO/MIRSD-PoD- 2/P/CIR/2023/90 dated June 15, 2023 read with clauses 1,2, 7 & 8 of the Code of Conduct as specified in Third Schedule under Regulation 24 (2) of the SEBI RA Regulations, 2014, against the Noticee stands established.

13. Offering assured returns –

13.1 It was observed from the Gap-up website, that the Noticee runs subscription plan in the name of “Index and Stock option”. In this page, it is highlighted that he has performance percentage of 75% accuracy. It was also observed that the Noticee has a handle @HarmonicsT in X (formerly Twitter) social media wherein he posts the stock recommendations. In this handle on January 25, 2024, he made reference to his past performance GLENMARK24JAN870PE- Update: 6.3 to 28 High!; 344% Return: 15730 rs single lot Profit; Power of WALL and PI Strategy; Free Money For All!; and on another post on February 24, 2024 in telegram Channel, 15.5 to 99.8 High | 59000+ Rs Single lot Profit; 5x Return; Target 15+ Done!; #Power of Breakfast; Free Money for All!; SUNPHARMA24FEB1480CE- Positional Update!. In view of the same, it was alleged that the Noticee had violated the provisions of Regulation 4(1) of SEBI, PFUTP Regulations, 2003 read with sections 12A(a),(b) & (c) of SEBI Act, 1992 and clause 1(c)(x) and (xii) of SEBI circular SEBI/HO/MIRSD/ MIRSD- PoD-2/P/CIR/2023/51 dated April 05, 2023 and clauses 1,2, 7 & 8 of the Code of Conduct as specified in Third Schedule under Regulation 24(2) of the RA Regulations, 2014.

13.2 As per the provisions of clause 1(c)(x) and (xii) of SEBI circular SEBI/HO/MIRSD/ MIRSD-PoD-2/P/CIR/2023/51 dated April 05, 2023, while issuing any advertisement, the RAs shall ensure compliance of the advertisement code prescribed in the said circular, which includes that the advertisement shall not contain reference to the past performance of the RA ; the advertisement shall not contain any promise or guarantee of assured or risk free return and shall not imply any assured or minimum returns or target return or any nomenclature that gives such impression or that it can generate returns with any level of assurance. As per the provisions of Regulation 4(1) of SEBI, PFUTP Regulations, 2003 read with sections 12A(a), (b) & (c) of SEBI Act, 1992, no person shall indulge in manipulative, fraudulent or unfair trade practice in securities markets.

13.3 Noticee has submitted that the mention of “75% accuracy” on the webpage of ‘Index and Stock option’ subscription plan was reference to the timing of the Noticee and nothing else. With respect to his posts on X (formerly Twitter) and telegram channel, Noticee submitted that the on a holistic reading, the messages would provide background and the context in which they were sent, and would evince a different meaning.

13.4 In this regard, it is noted that the mention of 75% accuracy on the webpage of the subscription plan, in the absence of any context, will generally be perceived as the accuracy of the recommendations of the research analyst. Thus, the mention of “75% accuracy” by the Noticee on the subscription web-page gives the impression that 75% of the Noticee’s recommendations can generate returns for his clients.

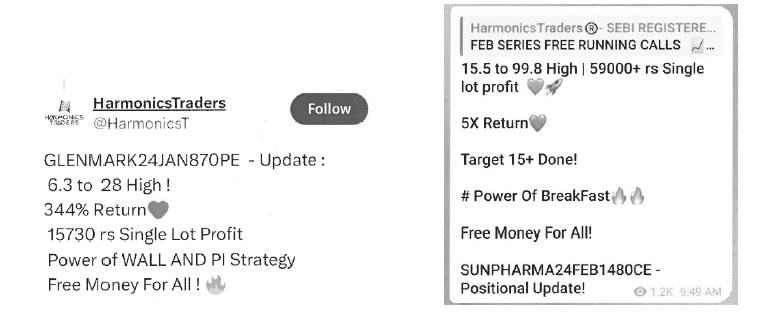

13.5 The Noticee’s posts on X (formerly Twitter) and Telegram channel are provided below for reference:

13.6 From the aforesaid screenshots, it is observed that the Noticee is providing updates of his previous recommendations where high returns were generated, and also used the phrases such as “free money for all”. By disseminating such selective information and phrases, the Noticee has given an impression that the clients can earn assured risk free returns. By referring to his past performance and stating free money for all and quoting less capital required, magnifying the returns on the capital employed, the Noticee has misled the investors and was luring the investors to join his subscription plans.

13.7 In view of the aforesaid, it is concluded that the Noticee has violated the provisions of Regulation 4(1) of SEBI, PFUTP Regulations, 2003 read with sections 12A(a),(b) & (c) of SEBI Act, 1992 and clause 1(c)(x) and (xii) of SEBI circular SEBI/HO/MIRSD/ MIRSD-PoD-2/P/CIR/2023/51 dated April 05, 2023 and clauses 1,2, 7 & 8 of the Code of Conduct as specified in Third Schedule under Regulation 24(2) of the RA Regulations, 2014.

14. To summarize the foregoing findings, Noticee has violated following provisions:

14.1 Clause 7 of the Code of Conduct as specified in Third Schedule under Regulation 24 (2) of the SEBI RA Regulations, 2014

14.2 Regulation 4(1) of SEBI, PFUTP Regulations, 2003 read with sections 12A(a),(b) & (c) of SEBI Act, 1992 and clause 1(c)(x) and (xii) of SEBI circular SEBI/HO/MIRSD/ MIRSD-PoD-2/P/CIR/2023/51 dated April 05, 2023 and clauses 1,2, 7 & 8 of the Code of Conduct as specified in Third Schedule under Regulation 24(2) of the RA Regulations, 2014.

ISSUE II – Do the violations, if any, attract penalty under Section 15EB and

Section 15HA of the SEBI Act, 1992?

15. It is noted that the above violations make the Noticee liable for monetary penalty under Section 15EB and Section 15HA of the SEBI Act, 1992, the text of which is reproduced hereunder:

SEBI Act, 1992

Penalty for default in case of investment adviser and research analyst.

15EB. Where an investment adviser or a research analyst fails to comply with the regulations made by the Board or directions issued by the Board, such investment adviser or research analyst shall be liable to penalty which shall not be less than one lakh rupees but which may extend to one lakh rupees for each day during which such failure continues subject to a maximum of one crore rupees.

Penalty for fraudulent and unfair trade practices.

15HA. If any person indulges in fraudulent and unfair trade practices relating to securities, he shall be liable to a penalty which shall not be less than five lakh rupees but which may extend to twenty-five crore rupees or three times the amount of profits made out of such practices, whichever is higher.

16. In context of the above, reference may be made to the observations of Hon’ble Supreme Court in the matter of Chairman, SEBI vs. Shriram Mutual Fund {[2006] 5 SCC 361} wherein the Hon’ble Court had observed: “In our considered opinion, penalty is attracted as soon as the contravention of the statutory obligation as contemplated by the Act and the Regulations is established and hence the intention of the parties committing such violation becomes wholly irrelevant A breach of civil obligation which attracts penalty in the nature of fine under the provisions of the Act and the Regulations would immediately attract the levy of penalty irrespective of the fact whether contravention must made by the defaulter with guilty intention or not. ”

ISSUE III – If so, what would be the monetary penalty that can be imposed taking into consideration the factors mentioned in Section 15J of SEBI Act, 1992?

17. While determining the quantum of penalty under Section 15EB and Section 15HA of the SEBI Act, 1992, it is important to consider the factors stipulated in Section 15J of the SEBI Act, 1992, which reads as under:

SEBI Act, 1992

15J While adjudging quantum of penalty under section 15-I, the adjudicating officer shall have due regard to the following factors, namely

- the amount of disproportionate gain or unfair advantage, wherever quantifiable, made as a result of the default;

- the amount of loss caused to an investor or group of investors as a result of the default;

- the repetitive nature of the default.

18. In the present matter, it is noted that no quantifiable figures are available to assess the disproportionate gain or unfair advantage made as a result of the defaults by Noticee. Further, from the material available on record, it may not be possible to ascertain the exact monetary loss to the investors /clients on account of default by Noticee. Further, as per the available records, it is observed that Noticee has not been penalised earlier for any of the aforesaid violations. Thus, violations are not repetitive in nature. While Noticee has now taken actions for KYC compliance, however, the fact cannot be ignored that as a SEBI registered intermediary, Noticee was under statutory obligation to comply with the applicable circulars, rules and regulations. The very purpose of the said regulations is to deter wrong doing and promote ethical conduct in the securities market. Further, the Noticee, by giving assurance of profit and returns, has misled the investors. Therefore, such noncompliance deserves and attracts imposition of suitable penalty.

ORDER

19. Having considered all the facts and circumstances of the case, the material available on record, the submissions made by Noticee and also the factors mentioned in Section 15J of the SEBI Act, 1992, and also taking into account judgment of the Hon’ble Supreme Court in SEBI vs. Bhavesh Pabari (2019) 5 SCC 90, in exercise of power conferred under Section 15-I of the SEBI Act,1992 read with Rule 5 of the SEBI Adjudication Rules, 1995, following penalty is hereby imposed upon the Noticee for the violations made hereunder.

Name of Noticee | Violation provisions | Penal Provisions | Penalty |

Mr Arun N (PAN No.: ARHPA4708R) | • Clause 7 of the Code of Conduct as specified in Third Schedule under Regulation 24 (2) of the SEBI RA Regulations, 2014 | Section 15EB of the SEBI Act, 1992 | 2,00,000/- (Rupees Two Lakh Only) |

Name of Noticee | Violation provisions | Penal Provisions | Penalty |

| • Regulation 4(1) of SEBI, PFUTP Regulations, 2003 read with sections 12A(a),(b) & (c) of SEBI Act, 1992 and clause 1(c)(x) and (xii) of SEBI circular SEBI/HO/MIRSD/ MIRSD-PoD- 2/P/CIR/2023/51 dated April 05, 2023 and clauses 1,2, 7 & 8 of the Code of Conduct as specified in Third Schedule under Regulation 24(2) of the RA Regulations, 2014. | Section 15HA of the SEBI Act, 1992 | ?5,00,000/- (Rupees Five Lakh Only) |

TOTAL | ?7,00,000/- (Rupees Seven Lakh Only) |

|

20. The Noticee shall remit / pay the said amount of penalty within 45 days of receipt of this order through online payment facility available on the website of SEBI, i.e. sebi.gov.in on the following path, by clicking on the payment link:

ENFORCEMENT ^ Orders ^ Orders of AO ^ PAY NOW.

21. In the event of failure to pay the said amount of penalty within 45 days of the receipt of this Order, SEBI may initiate consequential actions including but not limited to recovery proceedings under Section 28A of the SEBI Act, 1992 for realization of the said amount of penalty along with interest thereon, inter alia, by attachment and sale of movable and immovable properties.

22. In terms of Rule 6 of the SEBI Adjudication Rules, 1995, copy of this order is sent to the Noticee and also to the Securities and Exchange Board of India.

DATE: OCTOBER 24, 2024 BARNALI MUKHERJEE

PLACE: MUMBAI ADJUDICATING OFFICER